Debt Collection Lawsuits Continue to Flood State and Local Courts

Filings spiked in 2025 amid rising inflation and record household debt

With consumer prices rising throughout the country, Americans are feeling the pinch at the grocery store and the gas pump, and they are accumulating “survival debt”—liabilities accrued to pay for everyday expenses. As more people struggle to make ends meet and consumer debt reaches record highs, financial stress is rising.

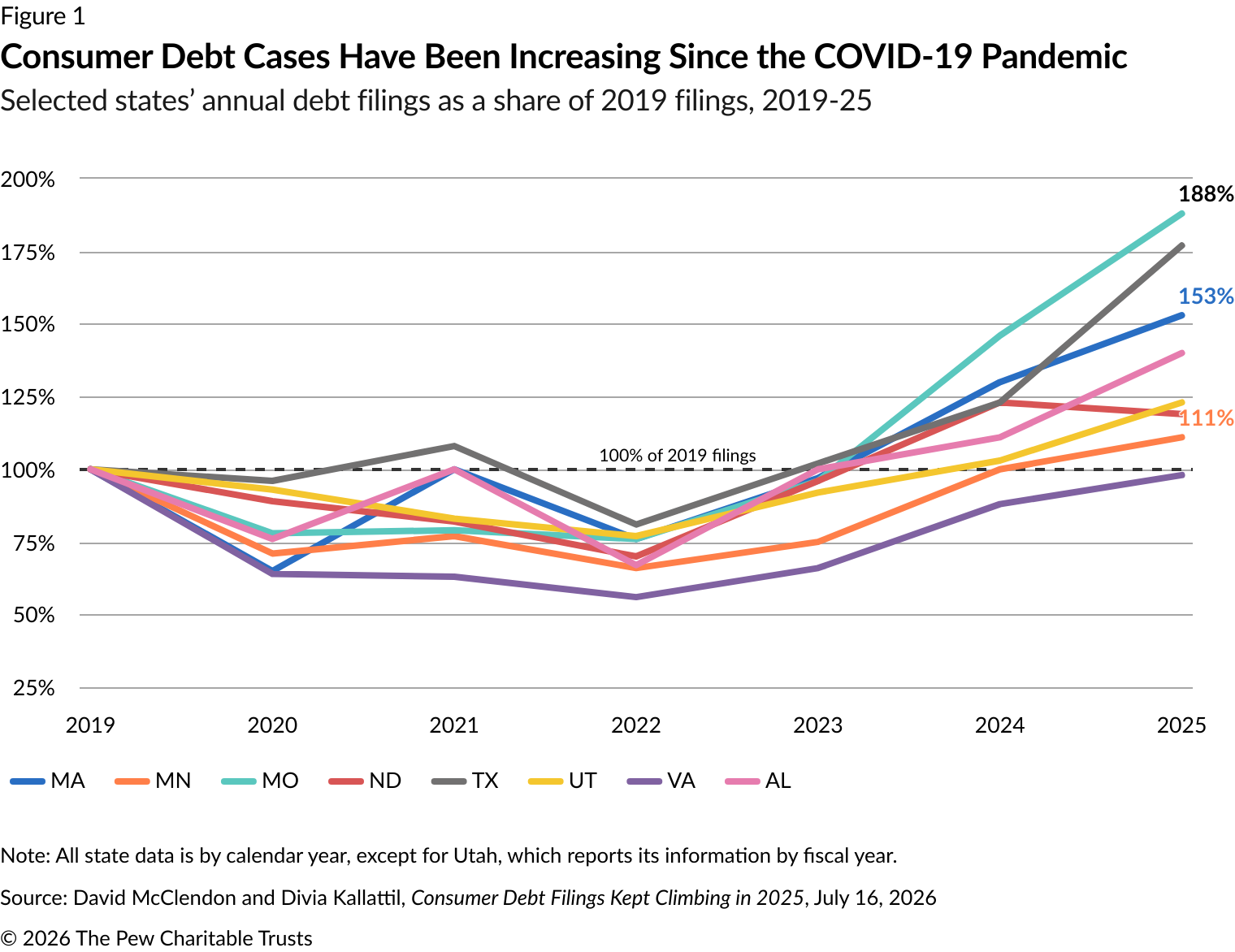

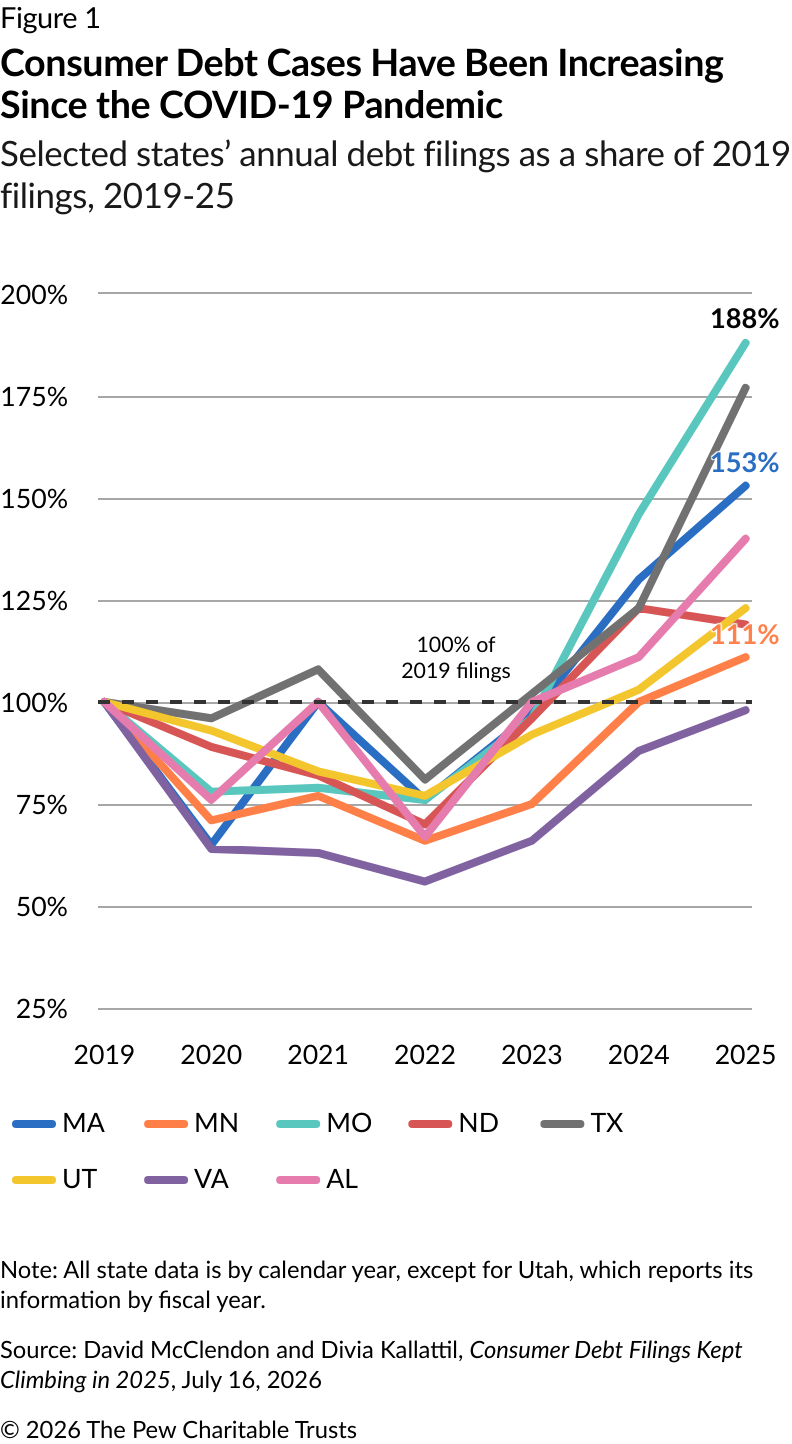

And this strain is showing up in state and local courts. A recent analysis from January Advisors finds that in 2025, debt lawsuits continued their upward trajectory, with filings growing rapidly in states and cities across the country. (See Figure 1.) For instance, in Utah, debt filings are on track to surpass their most recent peak, hit in the wake of the 2007-09 Great Recession; and in Alabama, they have already reached their highest level on record. These trends also hold true at the county level: St. Louis County, Missouri, and Suffolk County, Massachusetts, which is home to Boston, had 2025 debt filings of 198% and 168%, respectively, of their 2019 totals.

States can ensure that courts don’t exacerbate financial pressure

People who have been sued for debt encounter a complicated system and generally navigate it without a lawyer—less than 4% of people who have been sued have legal representation. And losing a debt lawsuit can have life-altering consequences: One man who was struggling to pay outstanding medical bills after his wife’s death unwittingly agreed to give the hospital $23,000 of the proceeds from the eventual sale of his house. And a woman in Michigan had 25% of her wages garnished for more than eight weeks because of a five-year-old utility bill she didn’t know she owed.

Some states have enacted reforms to help such struggling consumers pay off their outstanding debts. This spring, Virginia became the 14th state to automatically protect $1,000 of the money in consumers’ bank accounts from garnishment without requiring people to appear in court. Virginia’s protection does not forgive debt; rather, it allows consumers to continue paying off their debts while keeping enough money to also cover regular expenses.

Courts can ensure that rules are followed and processes are navigable

In addition to protecting against debilitating financial consequences of a lawsuit, state leaders can help ensure that people understand why they are being sued. This is particularly important because third-party debt buyers—firms that buy consumer debts from the original creditors and attempt to collect from the alleged borrowers—file a significant proportion of these cases, and so consumers may not easily recognize the party that is suing them. For instance, in the four states with available data, one company, LVNV Funding, filed nearly five times as many cases in 2025 as it did in 2019 and was responsible for 23% of all 2025 filings, according to the January Advisors analysis.

In 2026, two states have taken action to help courts validate claims and enable consumers to easily understand why they’re being sued, by whom, and what they need to do to defend themselves. Virginia and Washington passed legislation designed to increase transparency in debt collection lawsuits by requiring that filings include a recent monthly statement, chain of title, original loan contract, or other documentation to demonstrate that the plaintiff is suing the right person for the correct amount. These laws also compel the courts to confirm the accuracy and authenticity of the submitted documentation.

However, research from three states with similar requirements—California, Connecticut, and Minnesota—shows that despite these mandates, courts may not be thoroughly evaluating the submitted information and, as a result, may be issuing judgments on cases without merit.

To help improve and expedite review of debt documentation, some courts are turning to artificial intelligence (AI). For example, the Los Angeles Superior Court is working with Stanford’s Rhode Center and Legal Design Lab to use AI for debt claims, and preliminary evaluations show that AI-supported human review can reduce errors by 53% and time spent by 33% versus reviews done without AI assistance.

Practical strategies can aid courts, creditors, consumers

Court administrators and policymakers have critical roles to play in ensuring that every case on the debt docket is valid and that people who are sued have an opportunity to actively and effectively participate in their cases. States around the country are considering practical solutions that include:

- Following Virginia and Washington’s lead by passing legislation to ensure that courts and consumers have the relevant information about a lawsuit before a judgment is entered.

- Joining the 14 states that already have automatic post-judgment bank account protections in place.

- Supporting consumers who don’t have lawyers by simplifying procedures—such as by eliminating formal answer requirements and fees—to make it easier and less costly for unrepresented individuals to participate in court.

- Ensuring that people receive adequate notification when they’ve been sued, such as by requiring GPS verification when the consumer is served a lawsuit.

The current surge in debt collection lawsuits presents an urgent moment for policymakers throughout the country to ensure that all debt lawsuits have the required proof; to remove unnecessary barriers to consumer participation; and to provide appropriate protections for people facing a debt claim against them.

Lester Bird is a senior manager, Casey Chiappetta is an officer, and Eshaan Kawlra is a senior associate with The Pew Charitable Trusts’ courts and communities project.

People