Most Small Business Owners Support the Adoption of a State Automated Retirement Savings Program

Survey in Massachusetts, Pennsylvania, and Washington shows strong support across different business and personal demographics

Overview

A survey by The Pew Charitable Trusts indicates that small business owners across all demographics—including individual characteristics (e.g., political affiliation) and business characteristics (e.g., company size, age, and revenue)—support their state adopting an automated savings program (ASP) for retirement. These programs, also known as “auto-IRAs,” provide access to workplace retirement savings plans for many of the 47% of workers in the United States who lack it.1 To date, 17 states have adopted state ASPs.2

Employer support for auto-IRAs is important: While employers have almost no role in the programs, they facilitate payroll deductions for participating employees. Prior to OregonSaves—the first state ASP—opening in 2017, a nationwide Pew survey found strong employer support for the idea of a state program; a subsequent Pew survey of Oregon employers participating in OregonSaves found that employers generally supported the program.3

In 2023, Pew surveyed small employers, those with between 6 and 101 employees, about their support for these programs in three states where legislation has been introduced to adopt an auto-IRA: Massachusetts, Pennsylvania, and Washington.4 In total, 1,500 employers (500 in each state) completed the survey. (See the appendix for the survey methodology.)

Business owners in each state were strongly in favor, with 84% of respondents in Massachusetts, 76% in Pennsylvania, and 73% in Washington expressing support for their state starting an ASP.5 This brief takes a new look at the data from these states, focusing on the characteristics of the owners and the types of businesses they represent. Pew’s survey found broad support for program adoption across both personal and business characteristics.

Among the key findings:

- There is broad bipartisan support for the adoption of a state ASP, with majorities of Republican, Democratic, and independent business owners and leaders expressing support.

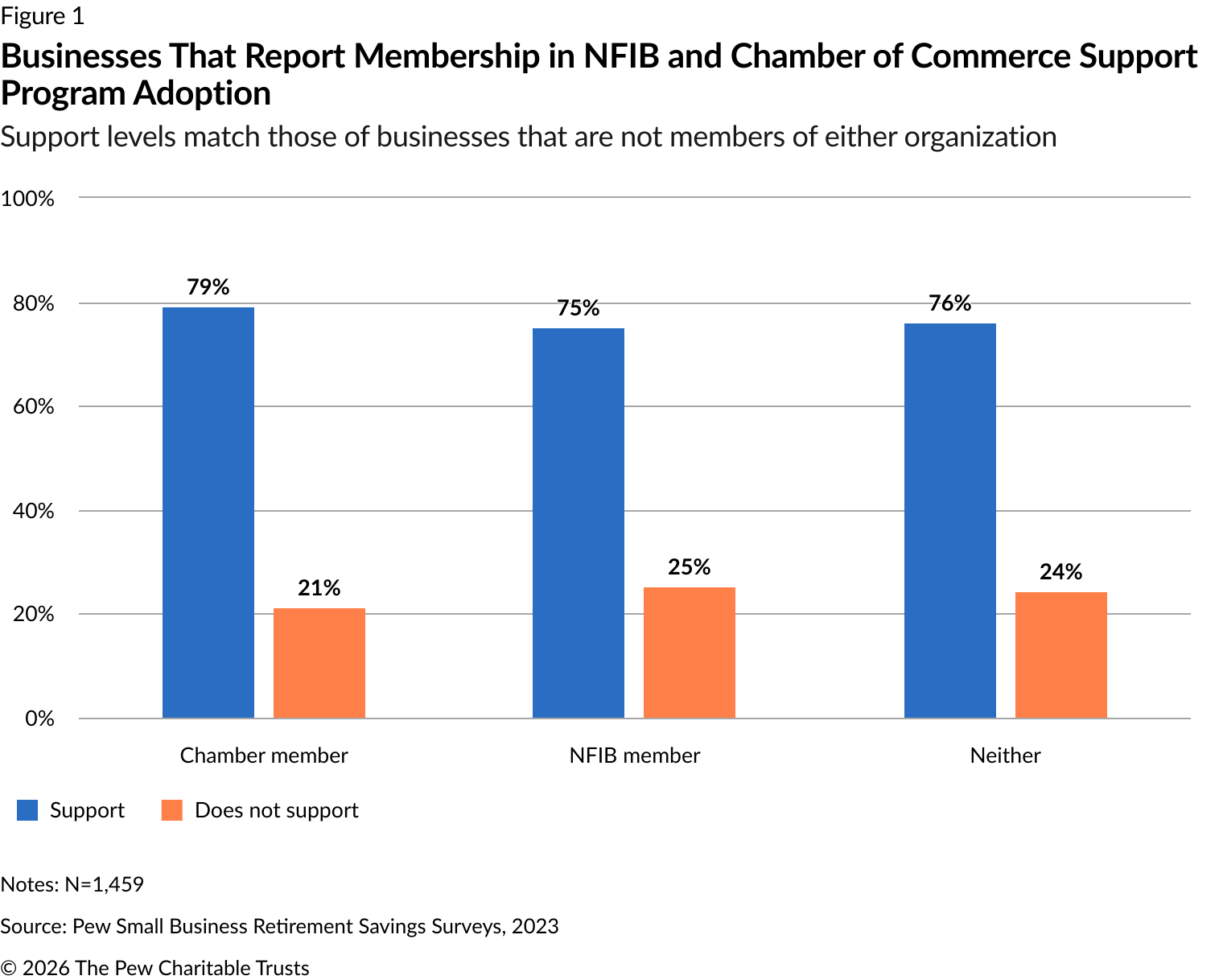

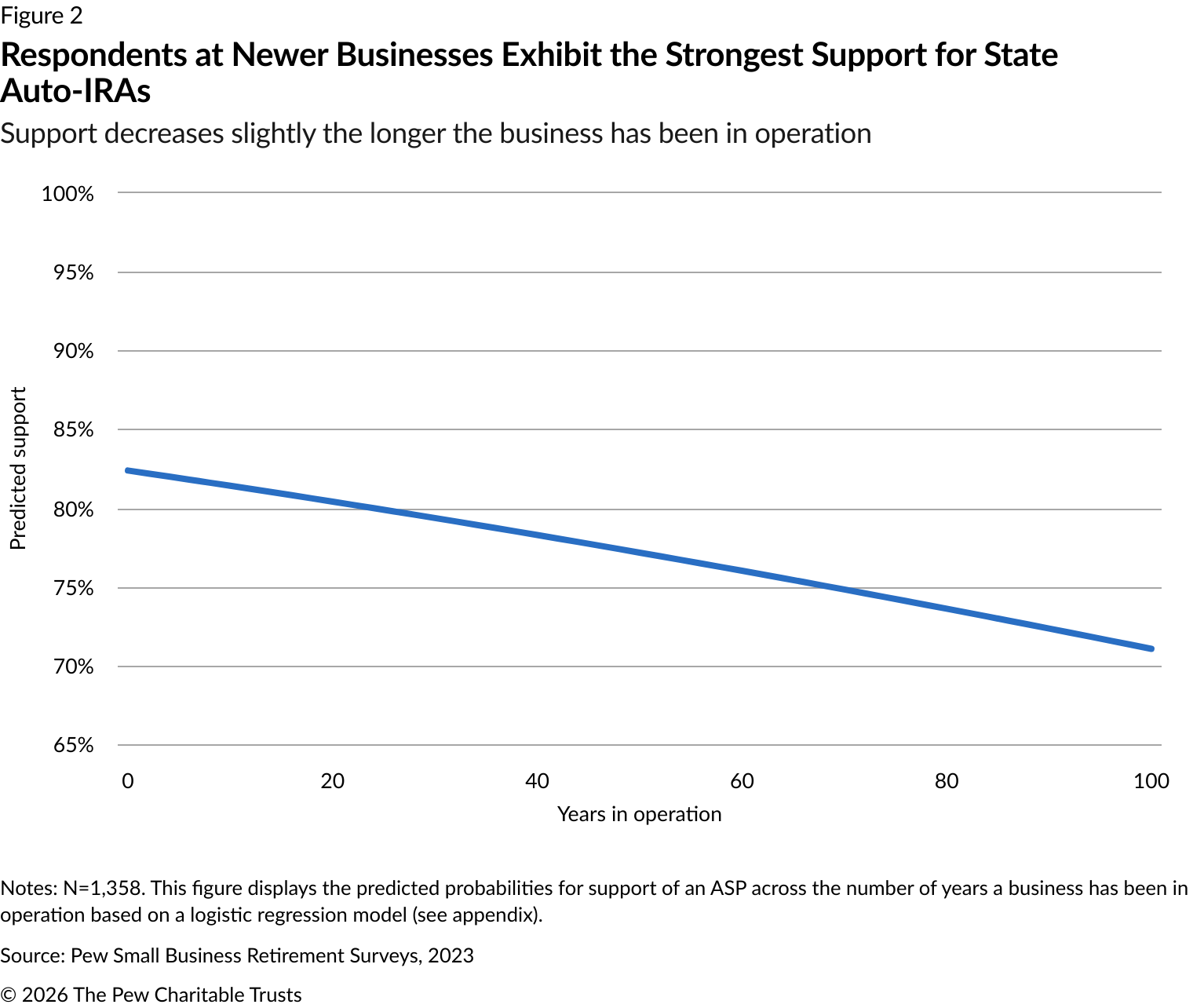

- Members of the state or local chamber of commerce (79%) and the National Federation of Independent Business (75%) support program adoption.

- While some individual respondent characteristics (such as age or conservative ideology) are associated with less support for program adoption, majorities across all groups expressed support.

- Statistically significant support for ASPs was associated with newer firms that had been in business a shorter amount of time (compared with others surveyed), had moderate annual business revenue, were in service producing industries, and did not already provide a retirement plan to their employees.

Support for ASP across business-related characteristics

When surveying employers, the researchers looked at membership in business associations; the size and age of the business; revenue; industry; and whether the business offered its own retirement savings plan.

Businesses without a retirement savings plan were only four percentage points more likely to support the adoption of a state program than businesses with a plan (79% versus 75%, respectively). While the difference was small, this factor was statistically significant in the regression analysis that assesses how change in support for the ASP is related to changes in other characteristics of firms and owners (see appendix); this may reflect the difficulty small employers face in trying to provide benefits to their employees. Businesses that were in service-producing industries, such as health care, hospitality, and retail, were more supportive of auto-IRAs than those producing physical goods, such as manufacturing and construction; the support was statistically significant and may reflect that businesses in service-producing industries have traditionally been more likely to offer retirement benefits than businesses in the goods-producing sector. Most other differences were small, and aside from the number of years a business has been in operation, the differences were not statistically significant.

Researchers asked respondents whether the business was a member of either the National Federation of Independent Business (NFIB) or the state or local chamber of commerce. Membership in a business association was not associated with any difference in support for program adoption. About 14% of respondents across the three states reported being a member of the NFIB and 35% were members of their state or local chamber of commerce. As shown in Figure 1, members of a chamber (79%) and the NFIB (75%) both expressed strong support for program adoption, and this level of support is in line with business owners without an affiliation with either organization (76%).

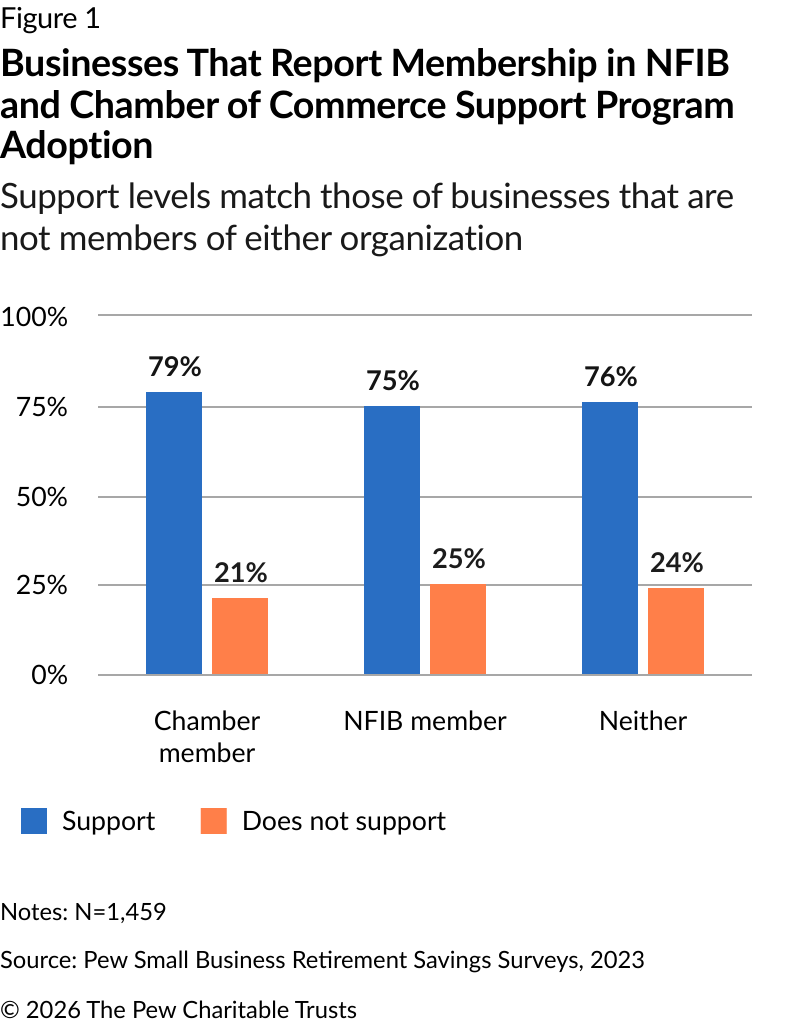

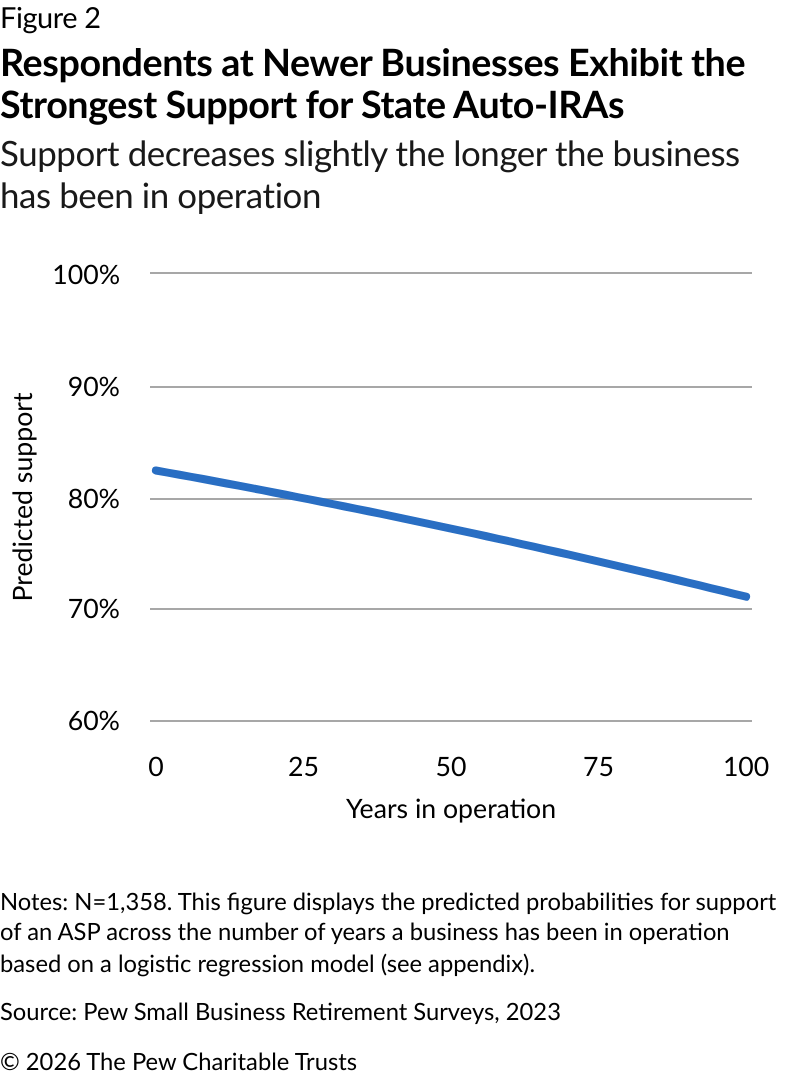

Younger firms were more likely to support ASPs than older firms, although all were generally supportive. (See Figure 2.) The difference between predicted support for a 6-year-old business (at the 10th percentile of ages in the sample) and a 67-year-old business (at the 90th percentile) is about seven percentage points (82% versus 75%, respectively, with numbers rounded). Younger firms may find it harder to afford private market retirement products such as 401(k) plans and therefore may be more likely to need auto-IRAs to compete with more established businesses. Older firms, meanwhile, may find that they do not need to offer retirement benefits to be able to compete in their market.

Individual business leader characteristics

Pew’s research found widespread support for state ASPs when surveying the positions of the survey respondents within their companies. More than half (54%) of respondents were the owner or co-owner of the business, while 46% were a decision-maker about employee benefits. Most respondents were highly supportive of adopting a state ASP, with 75% of owners and 81% of other decision-makers backing the program; holding all else equal in the predictive model, however, these differences are not statistically significant.

Researchers also analyzed potential differences across other individual demographics, such as the respondent’s sex, but found no significant differences in support between men and women.

Partisanship and ideology

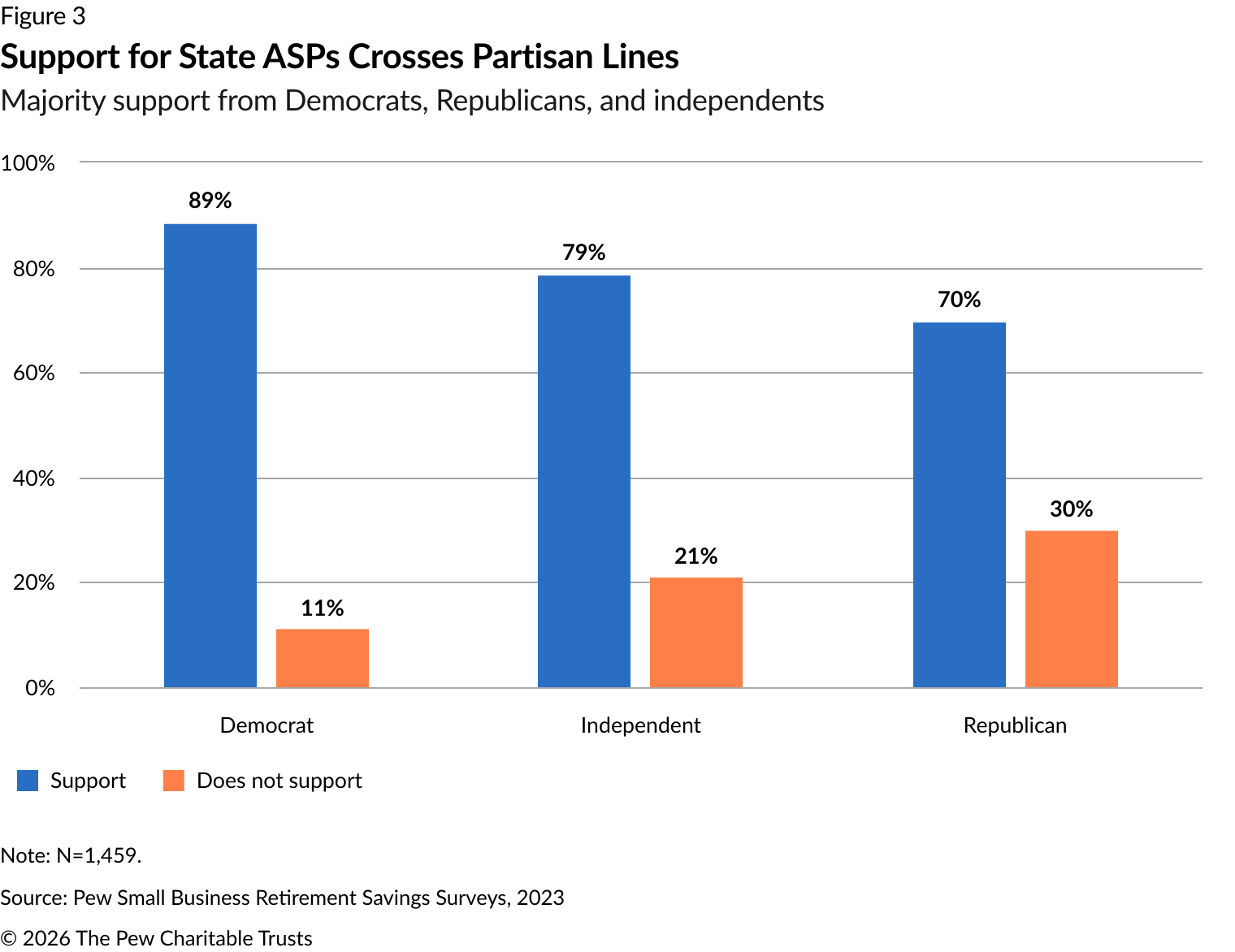

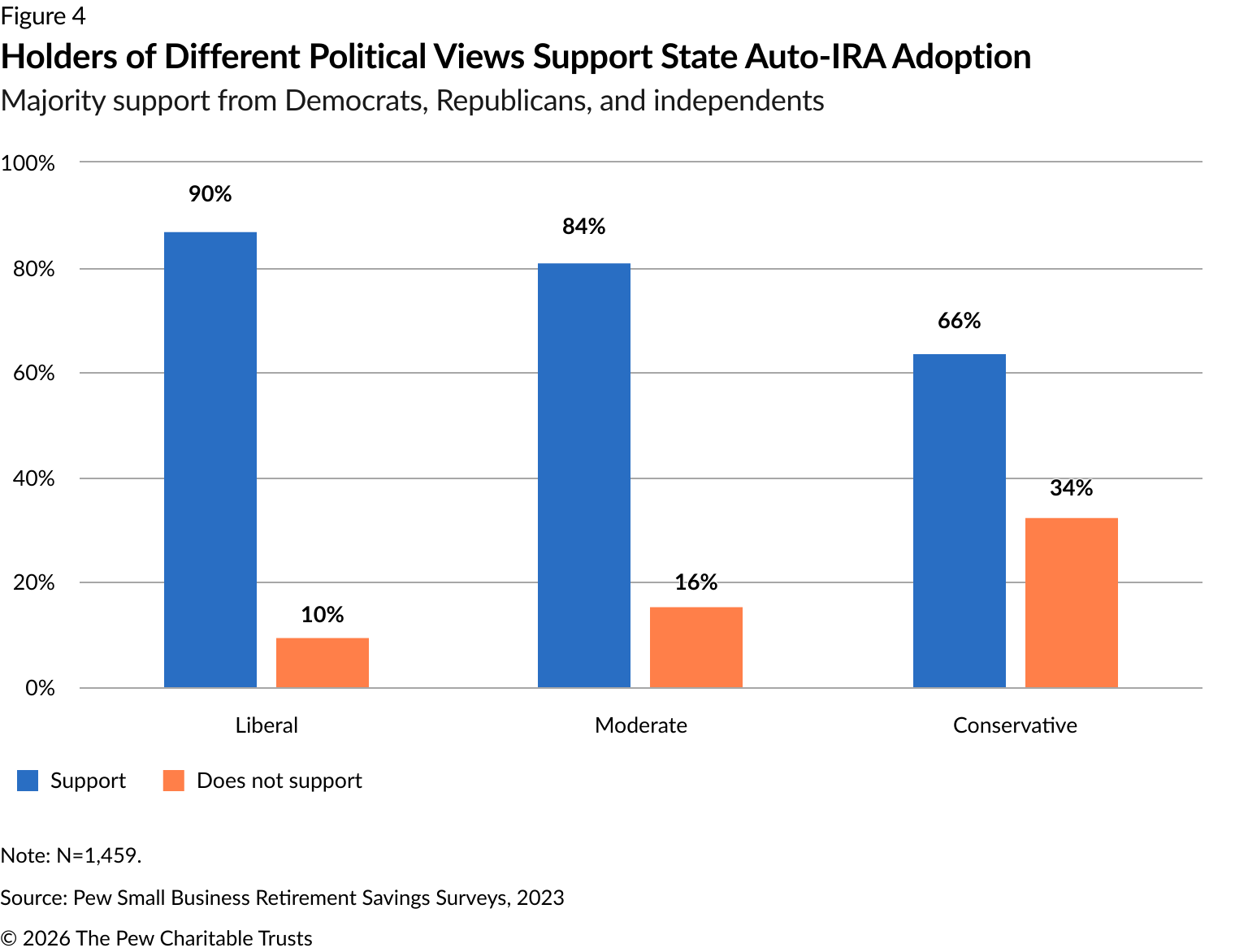

Majorities of business owners from across the political spectrum support the adoption of a state auto-IRA program in these three states: 70% of Republicans, 79% of independents, and 89% of Democrats supported the program. (See Figure 3.) The stronger support among independents and Democrats was statistically significant in the predictive model, holding all else equal.

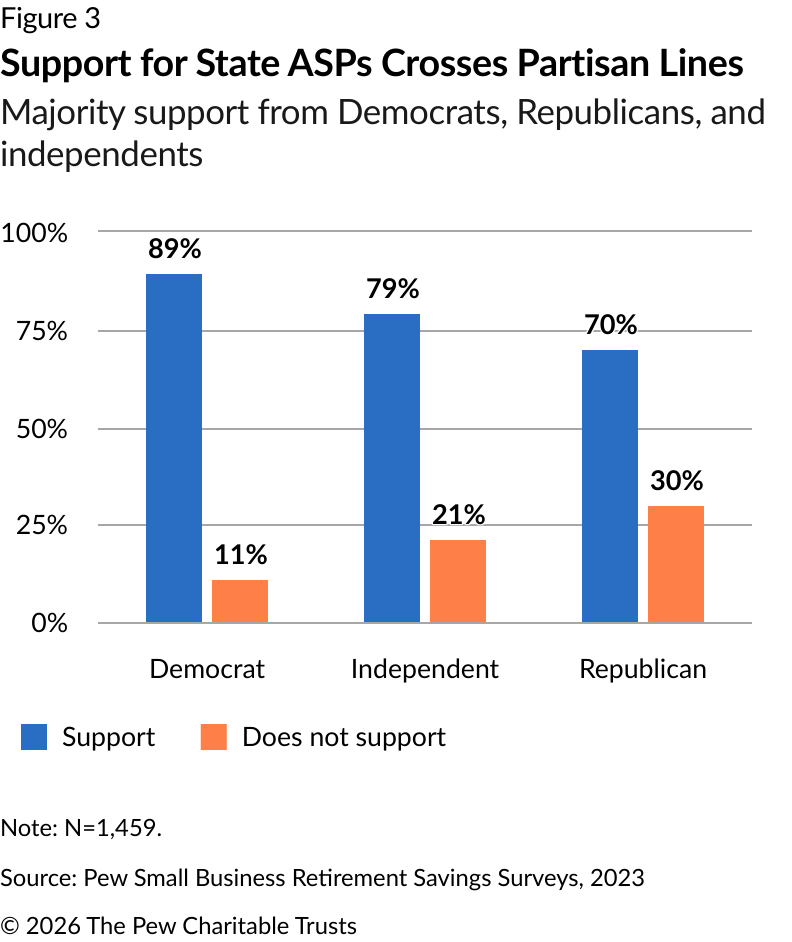

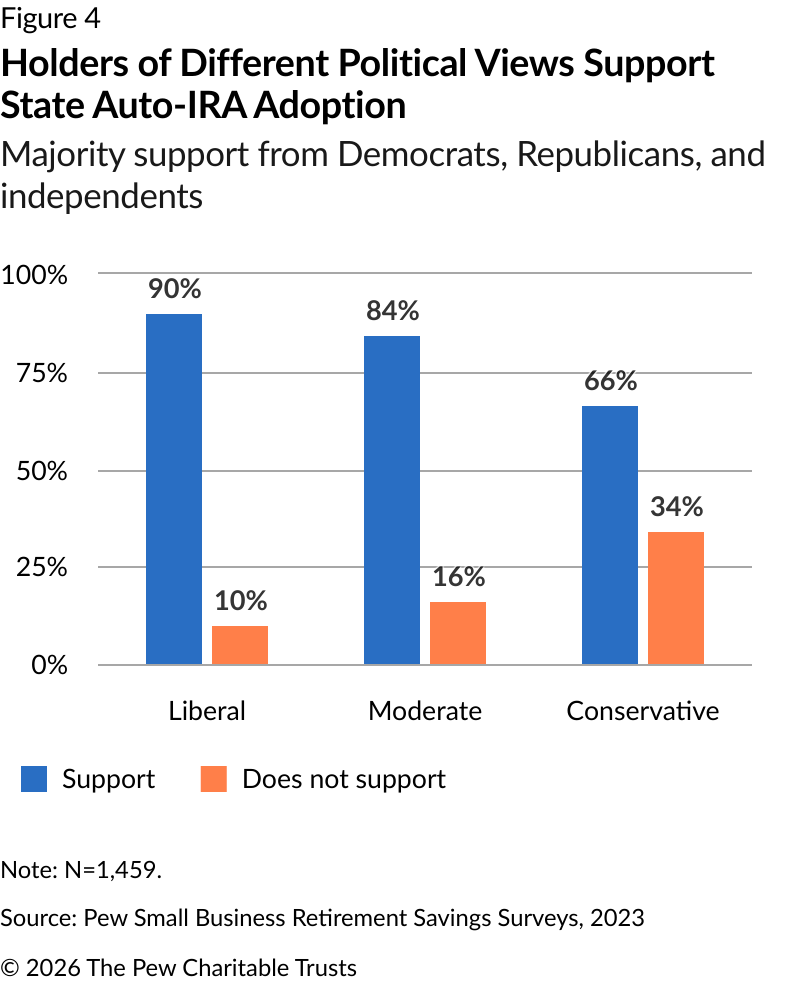

Political self-identification (liberal, conservative, and moderate) largely mirrors the trend for political affiliation. While 66% of conservative respondents said they support the adoption of a state ASP, support was higher among moderate (84%) and liberal (90%) respondents. (See Figure 4.) The lower support among conservative business owners compared with liberal and moderate owners was statistically significant in the predictive model; however, the difference between liberal and moderate support was not statistically significant.

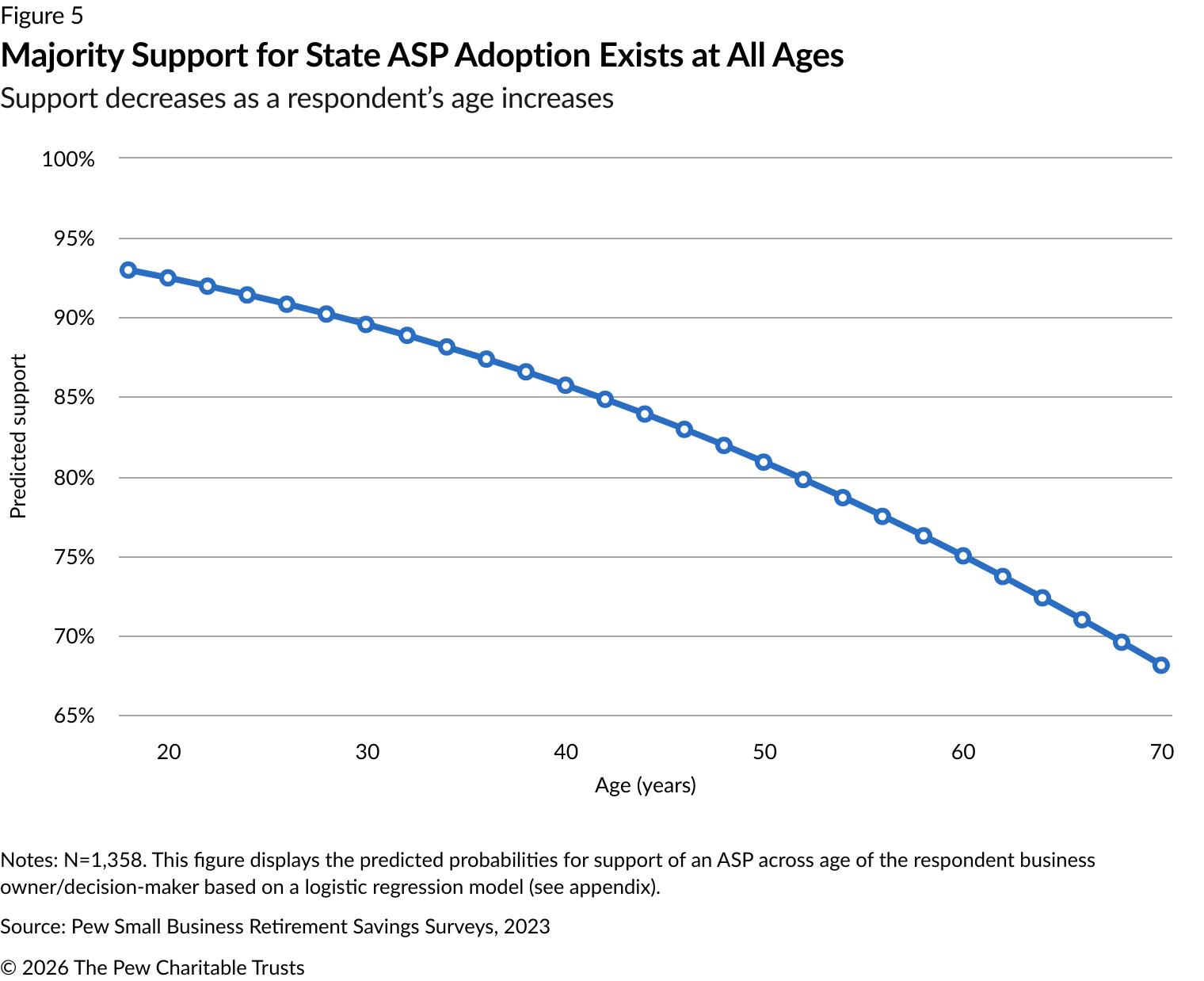

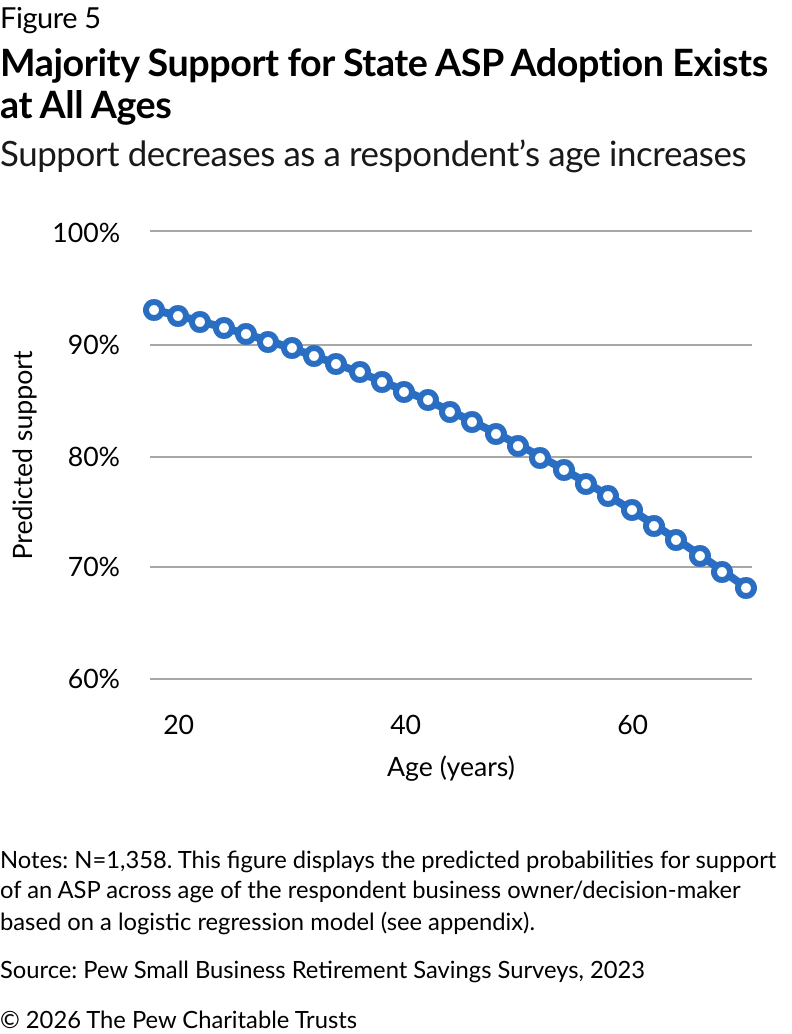

Age of the business owner or decision-maker

Substantial majorities of respondents of all ages expressed support for the program. As the age of a respondent increases, there is a slight decrease in support for adopting a state ASP; this relationship between age and support is statistically significant. (See Figure 5.) The difference between predicted support for a 34-year-old respondent (at the 10th percentile of ages in the sample) and a 68-year-old respondent (at the 90th percentile) is about 18 percentage points (88% versus 70%, respectively).

It is possible that individuals who are closer to retirement themselves do not see as much need for a program to help save for the future or to recruit and retain workers. The age of the individual business leader may also reflect the age of the firm, and as discussed above, younger firms are more supportive of ASPs than older firms, although a substantial majority of older firms support the programs.

Conclusion

Across all categories the researchers studied, a majority of small employers in the 2023 survey supported the adoption of state ASPs in Massachusetts, Pennsylvania, and Washington.

While support varied along some individual and business characteristics, it was nonetheless strong in each category, from a relative low of 66% among self-described conservatives to highs of 90% among liberals and 88% among younger respondents. Similarly, support among employers who belonged to business associations— state and local chambers and the NFIB—was almost as high as among employers who were not members. And support was high among the employers who arguably need these programs most: younger firms that do not provide retirement benefits.

State automated retirement savings programs have opened up savings opportunities to workers who have traditionally been left out of the system. In the 12 states with ASPs that are reporting program data, over one million workers have saved upwards of $2.75 billion in assets.6 As policymakers in other states consider proposals to expand access to workplace savings, these programs remain a promising path forward—and have strong support from small business owners.

Appendix

Methodology

The Pew Charitable Trusts engaged SSRS, a public opinion polling firm, to field the 2023 Small Business Retirement Savings Survey among small-business owners or decision-makers about employee benefits at companies with six to 101 employees, in three states: Massachusetts, Pennsylvania, and Washington.

SSRS and Clear Insights partnered to field the 2023 Small Business Retirement Savings Survey via telephone. The survey was conducted from July 27 to Sept. 28, 2023. A total of 500 business owners or decision-makers in each state completed the survey for a total sample size of 1,500. The results are representative of the population of small employers in each state. For this analysis, responses from each state are pooled together, with state fixed effects included in generating predicted probabilities.

Statistical regression analysis design

The main question of interest was support for adopting a state ASP. Respondents were asked whether they supported individual aspects of the program and then asked about support considering the program in its entirety: “Now I want you to think about all of these plan features together. Please tell me how much, if at all, you support the new retirement plan as a business owner or decision-maker. Do you …?” Response options included support, do not support, or don’t know. If a respondent said support, the interviewer asked: “Do you strongly or somewhat support?” Those response options were combined for the analysis. Those who responded “don’t know” or “not sure” were excluded from the analysis.

In this analysis, we have collapsed the business revenue category into fewer categories due to low cell counts at low levels of revenue. Industry categories were also collapsed due to low cell counts in individual industries; we have included whether a business is in a goods-producing or service-producing industry.

A respondent’s political party and ideology are strongly related to each other (chi-square test, p-value < 0.001). Therefore, separate models were run. Results for ideology are discussed in the text of this issue brief but the separate regression results are not presented here in the appendix. Only results for political parties are presented.

Predicted probabilities (presented in Figures 2 and 5) based on logistic regression model of program support (Model 3 in far-right column with full controls), were generated using Stata’s margins command.

Table A1

Logistic Regressions Predicting Probability of Supporting the Adoption of a State Automated Savings Program

Model 1 includes business-related characteristics, Model 2 adds controls for NFIB and chamber membership, and Model 3 adds controls for respondent characteristics

| Model 1 | Model 2 | Model 3 | ||||

|---|---|---|---|---|---|---|

| Variables | Odds ratio | Standard error | Odds ratio | Standard error | Odds ratio | Standard error |

|

Has a workplace retirement plan Yes No Don't Know |

(reference) 1.23 2.62 |

0.21 2.09 |

(refernce) 1.25 2.54 |

0.21 2.02 |

(reference) 1.48* 2.54 |

0.27 2.12 |

| Number of employees | 1.00 | 0.00 | 1.00 | 0.00 | 1.00 | 0.00 |

|

Business revenue Less than $100,000 $100,000 to less than $200,000 $200,000 to less than $500,000 $500,000 to less than $1 million $1 million or more Don't know Refused |

(reference) 1.60 2.20 1.50 1.18 0.68 0.36** |

0.65 0.92 0.53 0.36 0.27 0.13 |

(refernce) 1.59 2.21 1.48 1.16 0.59 0.34** |

0.65 0.93 0.53 0.35 0.24 0.12 |

(reference) 1.91 2.65* 1.60 1.31 0.65 0.48 |

0.84 1.21 0.61 0.44 0.29 0.19 |

| Years in operation | 0.99** | 0.00 | 0.99** | 0.00 | 0.99** | 0.00 |

|

Industry type Good-producing Service-producing Other |

(reference) 1.99** 0.87 |

0.35 0.43 |

(reference) 1.97** 0.87 |

V 0.35 0.42 |

(reference) 1.64** 1.13 |

0.31 0.61 |

|

Member of the NFIB No Yes Not sure |

- |

- |

(reference) 0.89 1.21 |

0.20 0.36 |

(reference) 1.02 0.86 |

0.25 0.28 |

|

Member of the chamber No Yes Not sure |

- |

- |

(reference) 1.26 1.63 |

0.23 0.60 |

(reference) 1.17 1.01 |

0.23 0.38 |

|

Respondent type Benefits decision-maker Owner of business |

- |

- |

- |

- |

(reference) 0.80 |

0.16 |

|

Respondent's political party Democrat Republican Independent Something else Don't know Refused |

- |

- |

- |

- |

(reference) 0.39** 0.52 0.50 0.34* 0.60 |

0.13 0.17 0.19 0.18 0.25 |

|

Respondent's sex Male Female Refused |

- |

- |

- |

- |

(reference) 1.13 0.55 |

0.24 0.47 |

| Respondent's age | - | - | - | - | 0.96** | 0.01 |

|

Respondent's state Massachusetts Pennsylvania Washington |

(reference) 0.61* 0.44** |

0.13 0.09 |

(reference) 0.60* 0.43** |

0.12 0.09 |

(reference) 0.67 0.35** |

0.15 0.08 |

|

Constant n = |

3.38** 1,448 |

1.23 |

3.20** 1,446 |

1.18 |

56.15** 1,358 |

38.47 |

Endnotes

- David John, Manita Rao, and Gary Koenig, “Payroll Deduction Retirement Programs Build Economic Security,” AARP Public Policy Institute, 2024, https://www.aarp.org/content/dam/aarp/ppi/topics/work-finances-retirement/financial-security-retirement/2024-payrolldeduction-retirement-fact-sheets/payroll-deduction-retirement-programs-build-economic-security.doi.10.26419-2fppi.00164.001.pdf.

- “State Programs 2026: Partnerships Expand, More Programs Launch, and the Focus Will Be the Enactment of More New State Programs and Initiatives,” Georgetown University Center for Retirement Initiatives, https://cri.georgetown.edu/states/.

- The Pew Charitable Trusts, “Employer Reactions to Leading Retirement Policy Ideas,” 2017, https://www.pew.org/en/research-andanalysis/reports/2017/07/employer-reactions-to-leading-retirement-policy-ideas. The Pew Charitable Trusts, “OregonSaves Auto-IRA Program Works for Employers,” 2021, https://www.pew.org/en/research-and-analysis/issue-briefs/2021/04/oregonsaves-auto-iraprogram-works-for-employers.

- At the time that we fielded the survey, Washington was considering adopting an automated retirement savings program. The state has since adopted one.

- The results in this analysis exclude respondents who said they “don’t know” or are “not sure” when asked about program support. “Small Businesses in Massachusetts Support State-Facilitated Retirement Savings Program,” Desiree A. Hung and John Scott, The Pew Charitable Trusts, Nov. 9, 2023, https://www.pew.org/en/research-and-analysis/articles/2023/11/09/small-businesses-in-massachusetts-support-state-facilitated-retirement-savings-program. “Small Businesses in Pennsylvania Support State-Facilitated Retirement Savings Program,” Desiree A. Hung and John Scott, The Pew Charitable Trusts, Nov. 30, 2023, https://www.pew.org/en/research-and-analysis/articles/2023/11/30/small-businesses-in-pennsylvania-support-state-facilitated-retirement-savings-program. “Small Businesses in Washington Support State-Facilitated Retirement Savings Program,” John Scott and Desiree A. Hung, The Pew Charitable Trusts, Nov. 15, 2023, https://www.pew.org/en/research-and-analysis/articles/2023/11/15/small-businesses-inwashington-support-state-facilitated-retirement-savings-program.

- For the most recent program data, see “State Program Performance Data,” Georgetown University Center for Retirement Initiatives, https://cri.georgetown.edu/states/state-data/current-year/.

People