Secondary Market Solutions Can Help Expand Small Mortgage Access

Fannie Mae and Freddie Mac have the chance to make homeownership possible for more Americans

Overview

Small mortgages—loans below $150,000—play a critical role in enabling affordable homeownership, particularly in lower-income and rural communities.1 But would-be homebuyers often find it difficult to obtain such a loan, even when they are otherwise well qualified.2 This difficulty stems largely from the economics of mortgage lending: Small mortgages cost about the same for lenders to originate as larger ones, but they generate less revenue.3 Without financial incentives, many lenders won’t issue small mortgages or will deprioritize them as part of their business model.4

Fannie Mae and Freddie Mac can help create that incentive. The two government-sponsored enterprises (GSEs) have a shared mission to provide liquidity, stability, and affordability to the U.S. housing market.5 The GSEs pursue that goal by buying millions of mortgages from lenders every year, packaging them into mortgage-backed securities, and guaranteeing cash flow to investors who buy those securities. Through this process, Fannie Mae and Freddie Mac directly compensate lenders for issuing loans that meet GSE standards, increasing the lenders’ financial flexibility and allowing them to make mortgages to new borrowers using fresh capital.

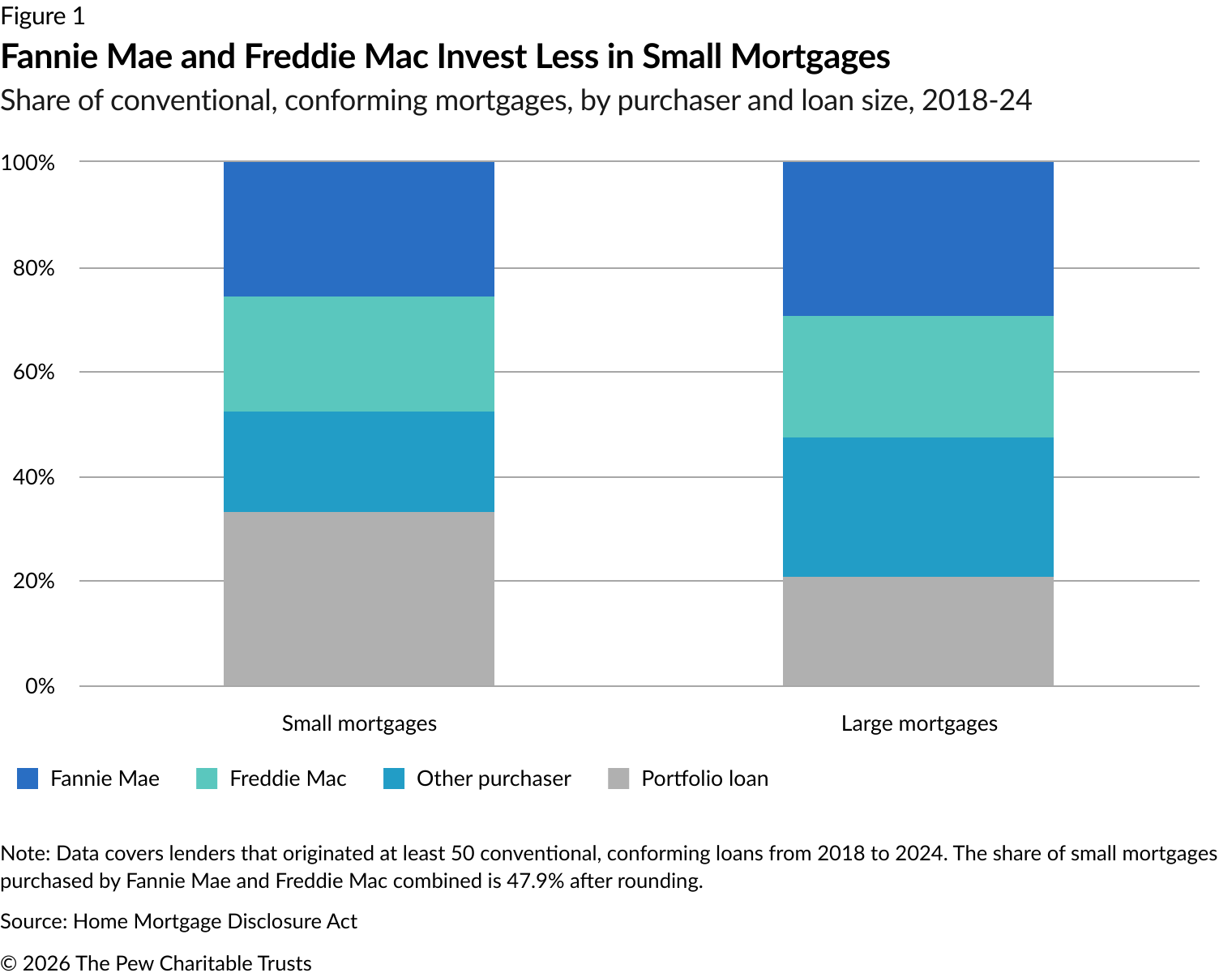

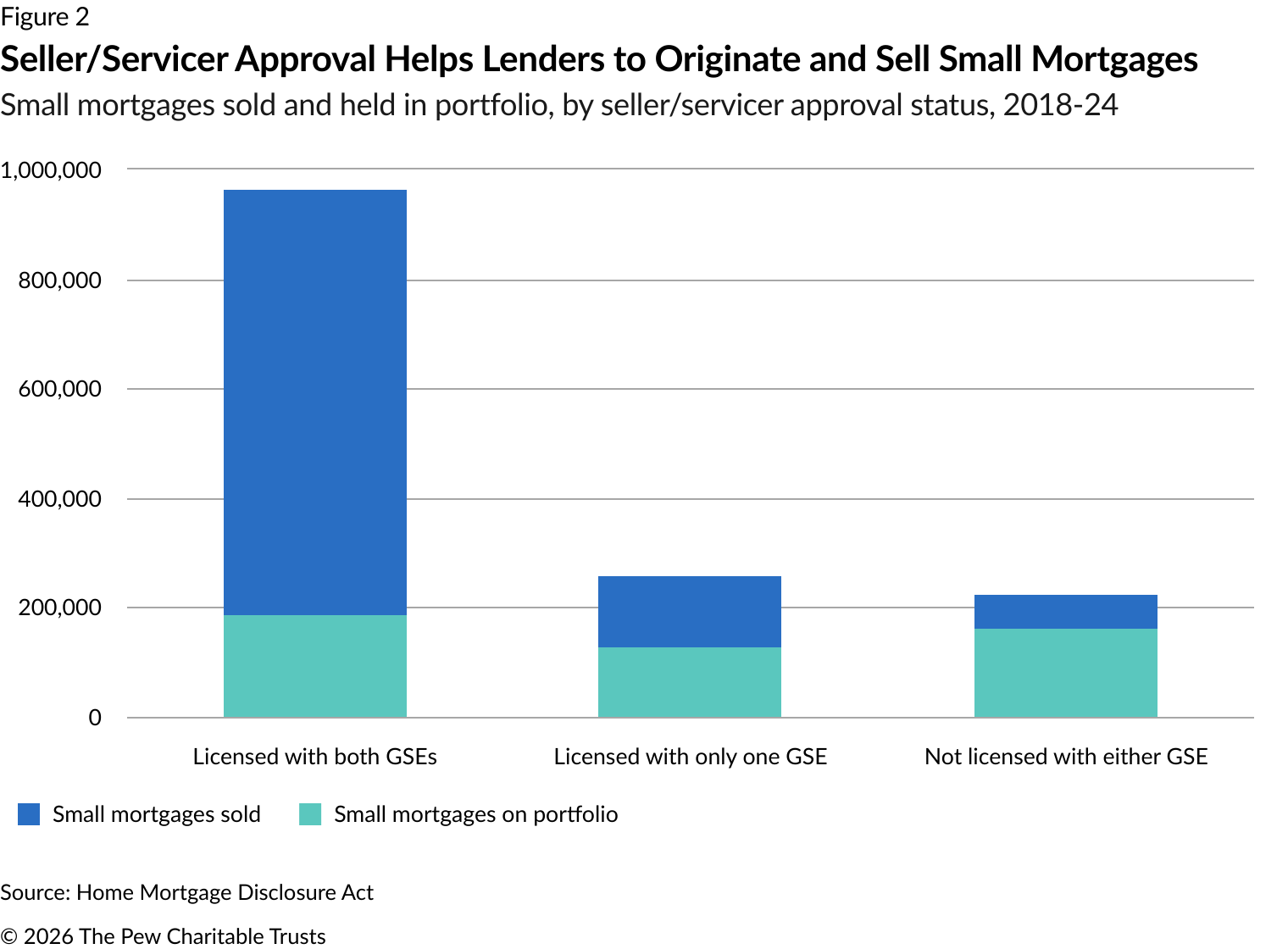

In recent years, however, the GSEs’ investment in small mortgages lagged that of larger loans. From 2018 to 2024, Fannie Mae and Freddie Mac collectively purchased 690,000 small mortgages (47.9% of all such loans), compared with 6.88 million larger ones (52.7%). Had the GSEs purchased a similar proportion of small and large mortgages, lenders could have sold an additional 70,000 small mortgages to the secondary market, freeing up $6.7 billion in lending capacity. Instead, these loans—many of which already conform to the GSEs’ standards—sit idle in lenders’ portfolios.

As Fannie Mae and Freddie Mac work to achieve their 2026-28 housing goals, federal officials should consider ways to expand the GSEs’ small mortgage investments.6 Research shows that small mortgages are often used by low- and moderate-income homebuyers, as well as those buying homes in lower-cost and rural parts of the country, but are typically no riskier than larger loans.7 Expanding GSE support for small mortgages would therefore advance affordable housing objectives without increasing risk or cost to the broader financial system.

To do this, the enterprises could try to reduce the costs or procedural requirements associated with becoming an approved seller/servicer. Currently, 80% of mortgage lenders are not approved to sell to Fannie Mae and/or Freddie Mac, with community banks and credit unions experiencing the greatest difficulties. In addition, the GSEs could revisit COVID-era restrictions on secondary market loan sales, giving lenders greater flexibility to recycle capital into new originations. Addressing one or both of these barriers would enable the GSEs to purchase more small mortgages, increasing revenue potential for lenders and expanding loan availability for more Americans.

The challenging economics of small mortgage lending

For many lenders, small mortgages are less profitable than larger loans. Mortgage costs—which include underwriting, appraisal, compliance, title search, and servicing setup—are roughly the same for a lender regardless of loan size. But mortgage revenue is often tied to the value of the loan: With a 1% loan origination fee, for example, a lender earns four times as much on a $400,000 mortgage as on a $100,000 loan. As a result, lenders earn lower profits on small mortgages, creating a disincentive to issue these loans.

The disincentives are magnified by regulatory requirements that make it more costly for lenders to hold loans on their balance sheets. In the wake of the 2007-09 Great Recession, new federal regulations strengthened capital and liquidity standards for banks and credit unions.8 These requirements increased the amount of capital that a lender must hold in reserve for every loan kept in its portfolio. While these reforms materially improved the resilience of individual institutions and the stability of the financial system as a whole, they also raised the cost of holding loans in portfolios, indirectly discouraging lenders from retaining larger volumes of mortgages on their balance sheets.

Independent mortgage companies—sometimes called independent mortgage banks—face a different challenge. Unlike a bank, credit union, or savings and loan, independent mortgage companies don’t accept deposits; they rely on short-term “warehouse” lines of credit to fund new loans and must sell those loans quickly to repay those lines and originate new mortgages.9 In addition, these companies must also meet net worth and liquidity requirements from Fannie Mae, Freddie Mac, and their warehouse lenders. As a result, independent mortgage companies have a strong incentive to sell loans rather than hold them.

The secondary mortgage market―particularly the GSEs—provides a crucial release valve for new mortgages. By purchasing loans and packaging them into mortgage-backed securities, Fannie Mae and Freddie Mac allow all types of lenders to convert illiquid mortgage assets into cash, freeing capital for new lending. This process helps banks comply with capital and liquidity requirements and enables independent mortgage banks to replenish their warehouse funding and sustain lending operations. In doing so, the GSEs help make small mortgage lending economically viable.

When this release valve is constrained, however, disruptions can ripple through the primary market. A clear example occurred in 2020, when the Federal Housing Finance Agency directed the GSEs to suspend bulk loan purchases and imposed a new requirement that all flow deliveries consist of loans no more than 6 months old.10 Although intended to address pandemic-related risk and capacity concerns, the suspension reduced balance sheet flexibility for portfolio lenders and limited a key liquidity outlet, illustrating how changes in GSE purchasing policies can materially affect lenders’ ability to originate and retain small mortgages.

The scale of the opportunity

Although Fannie Mae and Freddie Mac have explicit affordable housing goals, they continually invest less in small mortgages relative to larger ones. The GSEs collectively purchased 690,000 small mortgages from 2018 to 2024, which amounted to 47.9% of all conventional, conforming loans (those that meet the funding criteria and loan limits set by the Federal Housing Finance Agency) in that price range.11 In contrast, the GSEs bought 6.88 million larger loans over the same period, which accounted for 52.7% of that market. (See Figure 1.) If the GSEs purchased small mortgages at the same rate as larger loans, lenders could have sold an additional 70,000 loans valued at $6.7 billion.

Loans that are not purchased by the GSEs often remain on lenders’ balance sheets: 33% of small mortgages were held in original lenders’ portfolios from 2018 to 2024, compared with just 20.6% of larger loans. Most of the remaining mortgages were purchased by banks or other financial institutions, either to help satisfy federal or state Community Reinvestment Act obligations, which assess whether lenders are adequately meeting the credit needs of their local communities, or to serve as a revenue source to help fund their operations.

Sometimes, lenders hold loans in their portfolios because they don’t conform to federal standards and are therefore ineligible to be sold to Fannie Mae and Freddie Mac. However, The Pew Charitable Trusts’ research found that 182,000 of the 475,000 small mortgages held in the original lenders’ portfolios between 2018 and 2024 were underwritten using Desktop Underwriter or Loan Product Advisor, the automated underwriting systems offered by Fannie Mae and Freddie Mac. This finding suggests that more than a third of the small mortgages held in lenders’ portfolios already meet the GSEs’ underwriting standards and are therefore eligible for purchase.

Barriers to seller/servicer approval limit GSE participation

To sell mortgages directly to Fannie Mae or Freddie Mac, a lender must be approved as a seller/servicer and comply with the GSEs’ financial, operational, and compliance requirements. Lenders that are not approved may still access the GSE market indirectly by selling their loans to an approved third-party aggregator, which then sells the loans to Fannie Mae or Freddie Mac. While this indirect channel allows broader participation in the secondary market, it typically comes at a cost: Lenders have less flexibility about when and how to sell their loans, and they receive less in net revenue because the aggregator collects a percentage of the total.

Approval requirements nonetheless prevent many lenders from selling loans directly to Fannie Mae and Freddie Mac. Minimum net worth and liquidity thresholds, investments in technology and reporting systems, dedicated compliance and quality-control functions, and ongoing oversight obligations create significant fixed costs that do not scale with loan volume. As a result, smaller lenders are often unable to justify seller/servicer approval and instead retain loans on their balance sheets.

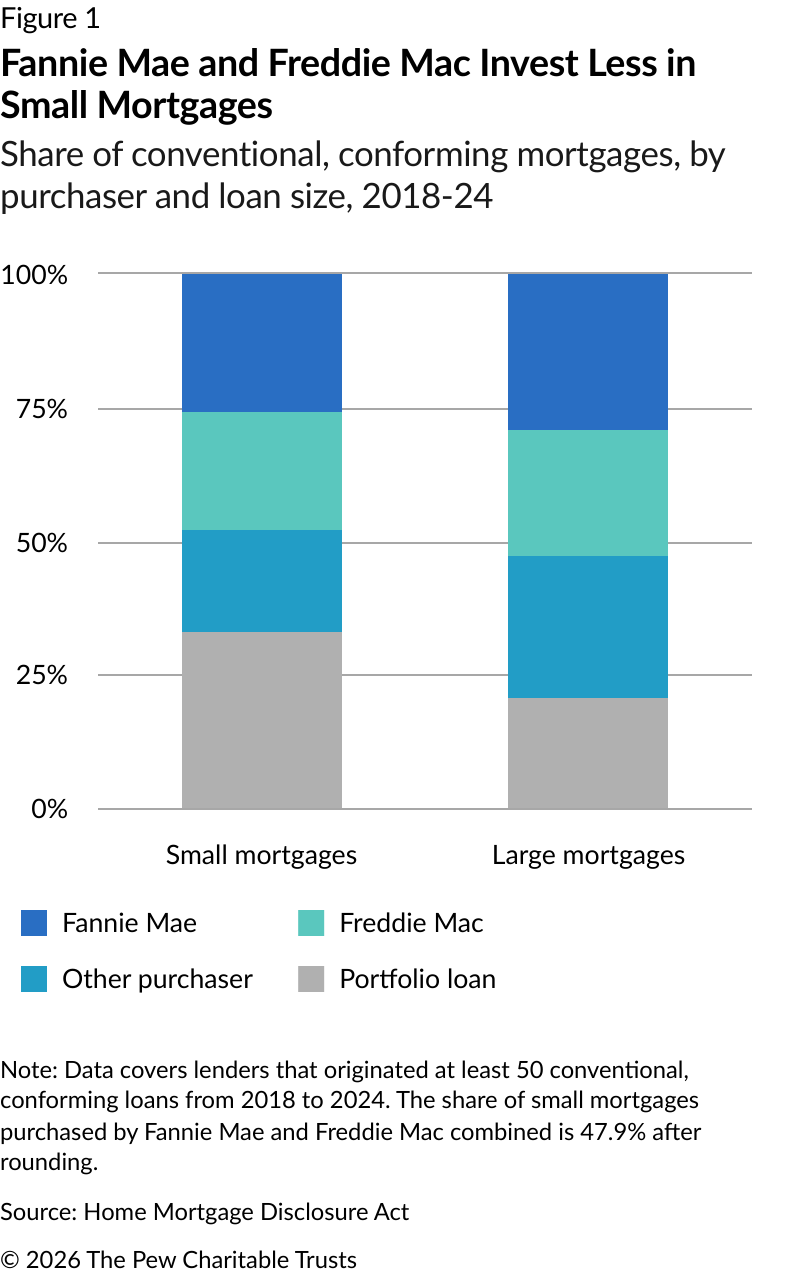

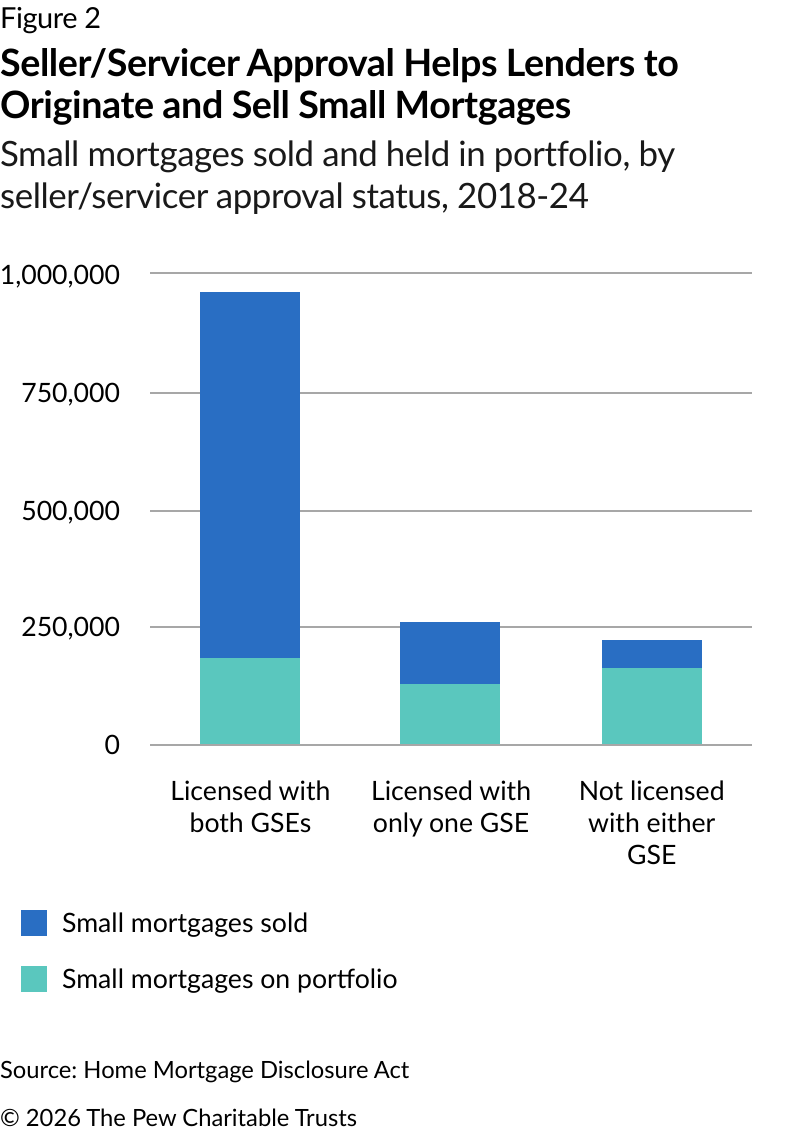

About 50% of lenders are not approved to sell loans to the GSEs. Among lenders that originated at least 50 conventional, conforming loans between 2018 and 2024, an estimated 1,840 were not approved seller/servicers with Fannie Mae or Freddie Mac, meaning they were ineligible to directly sell loans to either enterprise. These lenders combined issued more than 223,000 small mortgages during this period, but 162,000 of these loans—about 73%—remained in the original lenders’ portfolios. (See Figure 2.) Because this group of lenders originates so many small mortgages, expanding their access to the secondary mortgage market would increase the supply of loans eligible for purchase by a GSE. This change would, in turn, increase the ability of those lenders to issue additional small mortgages.

Approximately 30% of lenders are approved to sell to only one of the two GSEs. In 2024, an estimated 1,120 lenders were approved to sell to one of the two GSEs, which limited their selling options in the secondary market. These lenders issued roughly 258,000 small mortgages from 2018 to 2024 but retained half of these loans in their portfolios. Among the 129,000 loans sold, Fannie Mae and Freddie Mac purchased about 75,000 of them, while the remainder—around 54,000—were bought by banks, credit unions, insurance companies, and others.

About 20% of all mortgage lenders are approved to sell to both Fannie Mae and Freddie Mac. Despite including just 737 lenders, this group originated nearly two-thirds of all small mortgages between 2018 and 2024—about 961,000 loans. Their outsize role reflects, in part, the value of full access to the secondary market: Lenders that sell to both GSEs can more easily manage liquidity, recycle capital, and sustain higher levels of lending activity. Just 19% of small mortgages issued by this group of lenders were held in the original lenders’ portfolios during this period, in part because Fannie Mae and Freddie Mac bought roughly 615,000 of these loans.

What types of lenders are excluded from the GSE system?

Understanding which lenders fall into each approval category helps explain why so many small mortgages remain outside the GSE system.

Lenders without seller/servicer approval from either Fannie Mae or Freddie Mac tend to be smaller institutions with limited balance sheet capacity. (See Table 1.) Lenders in this category have a median of $592 million in assets and originate just 37 mortgages per year. Most are community banks and credit unions that serve local markets, and they are slightly more active in rural areas, where home prices and mortgage balances are lower. These lenders also originate a larger share of small mortgages than any other group, even though they issue few loans overall.

Lenders approved to sell either to Fannie Mae or Freddie Mac, but not both, fall in the middle of the spectrum. They are often regional banks or credit unions with greater assets and operational capacity than community institutions but smaller in scale than lenders with dual seller/servicer approval. Their access to a single GSE provides some liquidity support but limits their options when selling to the secondary market. Consequently, lenders approved to sell to a single GSE play an important but constrained role in originating small mortgages. This group issued a median of 97 mortgages per year from 2018 to 2024, and 14% of those loans were under $150,000.

Lenders approved to sell to both GSEs are as a group the largest institutions in the market, with a median $3.1 billion in assets. This group includes national banks and high-volume independent mortgage companies. Their size makes them better equipped to meet the financial and compliance requirements that come with seller/servicer approval. Although lenders with dual seller/servicer approval originate a majority of small mortgages in the United States, these loans make up a smaller share of total originations (8%) than with smaller lenders. Their scale and secondary market access enable them to recycle capital efficiently, but they focus heavily on higher-balance loans in urban and suburban markets.

Table 1

Small Lenders Are Often Excluded From the Secondary Market

Characteristics of lenders, by seller/servicer status, 2018-24

| Total | Sells loans to both Fannie Mae and Freddie Mac | Sells loans to either Fannie Mae or Freddie Mac | Doesn’t sell loans to Fannie Mae or Freddie Mac | ||

|---|---|---|---|---|---|

| Lender count | 3,697 | 737 | 1,120 | 1,840 | |

| Community bank | 1,832 | 199 | 541 | 1,092 | |

| Credit union | 1,092 | 148 | 454 | 490 | |

| Independent mortgage company | 652 | 319 | 110 | 223 | |

| National bank | 121 | 71 | 15 | 35 | |

| Median asset per lender | $814.8 million | $3.1 billion | $976.9 million | $591.8 million | |

| Median annual loans per lender | 71 | 580 | 97 | 37 | |

| Median share of loans in rural areas | 9% | 7% | 9% | 11% | |

| Median share of loans under $150,000 | 15% | 8% | 14% | 21% | |

Note: Data includes only lenders who originated at least 50 conventional, conforming mortgages from 2018 to 2024.

Source: Home Mortgage Disclosure Act, 2018-24

Policy roadmap: Expanding secondary market access

Fannie Mae and Freddie Mac could take several targeted actions that would improve liquidity for lenders and small mortgage access for borrowers, while also helping them achieve their affordable housing goals:

- Identify and address barriers to seller/servicer approval. Roughly 80% of mortgage lenders lack the ability to sell loans to Fannie Mae or Freddie Mac, limiting their access to the secondary market and thus their ability to originate additional mortgages. This includes thousands of small community banks and credit unions, which have an outsize footprint in rural areas. The GSEs should examine why they partner with so few of these lenders and review their seller/servicer guidelines to ensure they do not unintentionally exclude smaller institutions. Expanding eligibility would unlock new small mortgage supply and enable the GSEs to better meet their stated mission.

- Revisit restrictions on how loans can be sold into the secondary market. Since 2020, Fannie Mae and Freddie Mac have restricted two key pathways through which lenders sell loans into the secondary market. Bulk purchases—negotiated transactions in which a lender sells a large quantity of portfolio loans to a GSE at once—were suspended during the pandemic and have not been reinstated. Flow delivery—the routine, loan-by-loan sales that represent the primary channel for most lenders—was simultaneously restricted to loans no more than 6 months old. Together, these changes reduced lenders’ ability to offload mortgages from their balance sheets and inhibited their ability to recycle capital into new loans.

- Expand dedicated pools of small mortgages. Research shows that small mortgage borrowers repay their loans more slowly, on average, than borrowers who take out larger loans. This feature is attractive to investors who desire stable, predictable returns. Fannie Mae and Freddie Mac could therefore consider offering more mortgage-backed securities composed entirely of small mortgages. The GSEs already issue securities with average loan balances as low as $85,000 that perform well and exhibit strong investor demand.12 Expanding these offerings could enable lenders, investors, and the GSEs to better support affordable homeownership, especially in low-income and rural communities.

Conclusion

Small mortgages are vital to affordable homeownership in much of the United States, but they are underserved by the secondary mortgage market. Fannie Mae and Freddie Mac excel at purchasing larger mortgages but have historically purchased a lesser share of small mortgages, with the shortfall reaching over 70,000 loans and $6.7 billion between 2018 and 2024. The lack of GSE investment has reduced financial incentives for lenders to issue small mortgages and limited borrowers’ access to safe and affordable financing.

But small changes could make a big difference in improving secondary market access. By identifying and addressing barriers to seller/servicer approval, authorizing purchases of seasoned small mortgages, and issuing more mortgage-backed securities composed entirely of small mortgages, Fannie Mae and Freddie Mac could help stimulate this critical market segment. These actions would free up capital for lenders, expand access to affordable credit, and reaffirm the GSEs’ public mission of promoting liquidity, stability, and affordability in every corner of the mortgage market.

Endnotes

- Adam Staveski, "Small Mortgages Offer Opportunity to Invest in Rural Communities," The Pew Charitable Trusts, 2024, https://www.pew.org/en/research-and-analysis/articles/2024/12/17/small-mortgages-offer-opportunity-to-invest-in-rural-communities.

- Laurie Goodman, Bing Bai, and Wei Li, "Real Denial Rates: A Better Way to Look at Who Is Receiving Mortgage Credit," Urban Institute, 2018, https://www.urban.org/sites/default/files/publication/98823/real_denial_rates_1.pdf.

- Mike Fratantoni et al., "How Do Mortgage Revenues, Costs and Profitability Vary by Loan Balance? An Analysis Using Benchmarking Data," Mortgage Bankers Association, 2023, https://www.mba.org/docs/default-source/research-and-forecasts/research-white-papers/impact-of-loan-size-on-profits-9-7-2023.pdf.

- The Pew Charitable Trusts, "Small Mortgages Are Too Hard to Get," 2023, https://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2023/06/small-mortgages-are-too-hard-to-get.

- "About Fannie Mae & Freddie Mac," Federal Housing Finance Agency, https://www.fhfa.gov/about-fannie-mae-freddie-mac.

- Federal Housing Finance Agency, 2026–2028 Enterprise Housing Goals, 90 Fed. Reg. 59948 (Dec. 23, 2025), https://www.federalregister.gov/documents/2025/12/23/2025-23746/2026-2028-enterprise-housing-goals.

- "The Lending Hole at the Bottom of the Homeownership Market," Sabiha Zainulbhai et al., New America, https://d1y8sb8igg2f8e.cloudfront.net/documents/The_Lending_Hole_at_the_Bottom_of_the_Homeownership_Market_11-2021.pdf. Amalie Zinn et al., "Improving the Availability of Small Mortgage Loans," Urban Institute, 2022, https://www.urban.org/sites/default/files/2022-12/Improving%20the%20Availability%20of%20Small%20Mortgage%20Loans.pdf. "3 Major Obstacles Limit Rural Homeownership," Adam Staveski, The Pew Charitable Trusts, https://www.pew.org/en/research-and-analysis/articles/2024/12/19/3-major-obstacles-limit-rural-homeownership.

- "Understanding the Current Regulatory Capital Requirements Applicable to US Banks," Guowei Zhang and Peter Ryan, Securities Industry and Financial Markets Association, https://www.sifma.org/news/blog/understanding-the-current-regulatory-capital-requirements-applicable-to-us-banks. "Risk-Based Capital Rule Resources," National Credit Union Administration, 2022, https://ncua.gov/regulation-supervision/regulatory-compliance-resources/risk-based-capital-rule-resources.

- "Warehouse Lending Fact Sheet," Mortgage Bankers Association, https://www.mba.org/docs/default-source/uploadedfiles/policy/22841-mba-warehouse-lending-brochure-pages.pdf.

- "Subject: Selling Requirements and Guidance Related to COVID-19," Freddie Mac, May 5, 2020, https://guide.freddiemac.com/ci/okcsFattach/get/1003810_7. Fannie Mae, Lender Letter (LL-2020-03) to All Fannie Mae Single-Family Sellers: Impact of COVID-19 on Originations, updated Dec. 10, 2020, https://singlefamily.fanniemae.com/media/22316/display.

- "FHFA Conforming Loan Limit Values," Federal Housing Finance Agency, Nov. 25, 2025, https://www.fhfa.gov/data/conforming-loan-limit.

- Federal Housing Finance Agency, "FHFA Statistics: Securitization of Manufactured Housing Loans in Enterprise Portfolios," Oct. 9, 2024, https://www.fhfa.gov/blog/statistics/securitization-of-manufactured-housing-loans-in-enterprise-portfolios. "Low Loan Balance 15-Year Pools Have Excellent Convexity," John Killian, Santander US Capital Markets LLC, 2018, https://portfolio-strategy.apsec.com/2018/10/26/low-loan-balance-15-year-pools-have-excellent-convexity.

People