Why Veterans Borrow Student Loans Despite Access to Robust Education Benefits

Substantial debt can jeopardize veterans’ post-military transitions

Overview

The Post-9/11 GI Bill offers a robust set of education benefits designed to help veterans make successful transitions into post-military life and careers. For those with 100% eligibility, it covers in-state tuition and fees at public schools or up to $29,921 annually at private institutions, provides a monthly housing allowance, and includes a stipend to defray the cost of books and supplies.1 Unsurprisingly, this benefit has proved to be exceptionally popular, with over 400,000 veterans tapping into it during fiscal year 2024.2

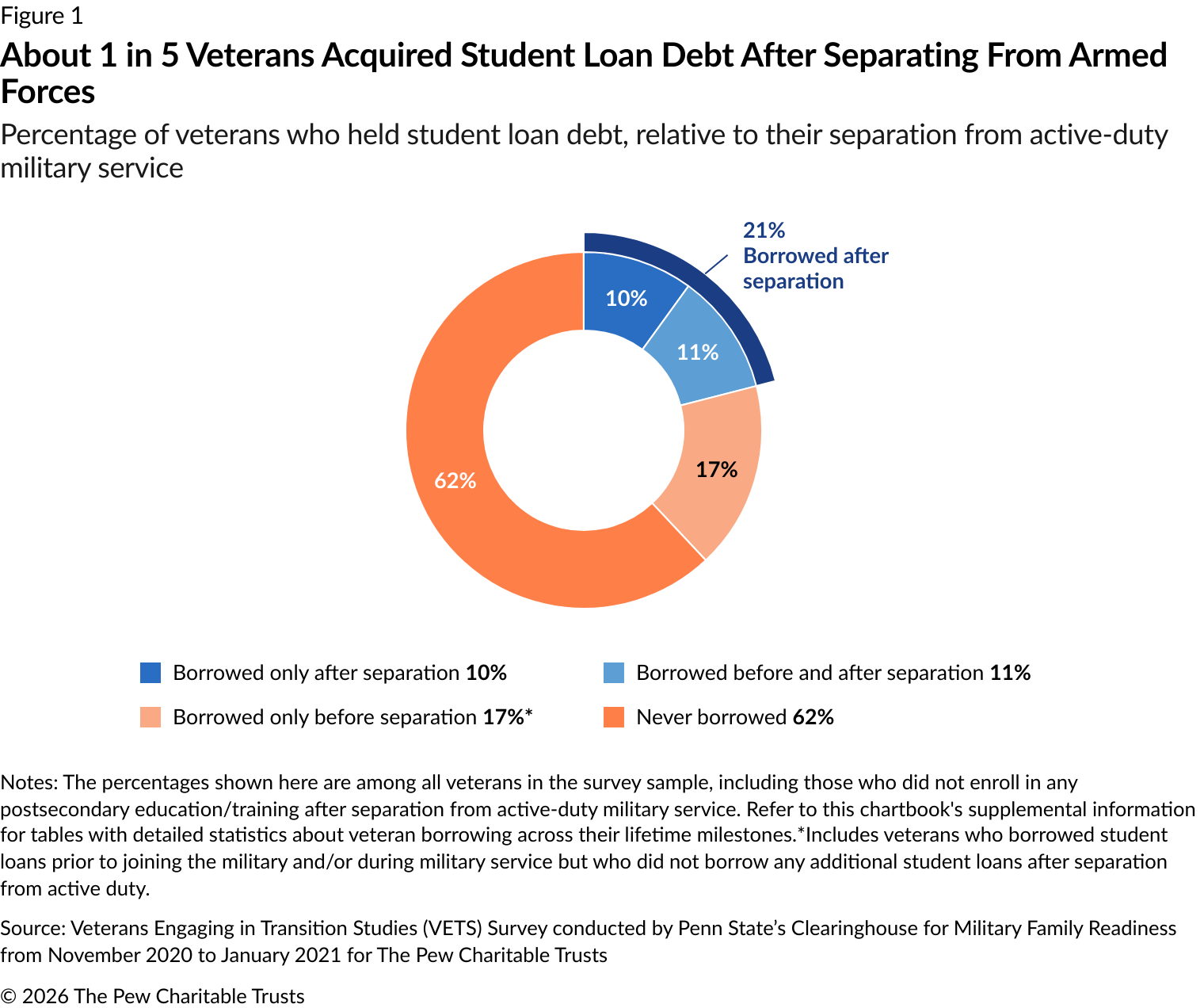

However, a prior analysis from The Pew Charitable Trusts revealed an apparent paradox: Despite having access to the Post-9/11 GI Bill, undergraduate student veterans borrowed a median amount of $8,000 in student loans during the 2015-16 school year, whereas their nonveteran counterparts borrowed a median of $7,500.3 Furthermore, about 1 in 5 veterans (21%) borrowed an average of $22,597 in student loans in the first four years of their post-military transitions.4 And this accumulation of student loan debt could hamper some veterans’ military-to-civilian transitions. Two out of every three veterans who took out student loans after leaving the military reported feeling stress as a result of their loans.

This chartbook focuses on the roughly 1 in 5 veterans who took out new student loans after separating from active-duty military service to understand why they borrowed despite having access to benefits from the Post-9/11 GI Bill.5 Our analysis is based on data drawn from a 2020-21 nationally representative survey of 3,180 veterans that asked about their transition from military to civilian life during 2016-20. Key findings include:

- Student veterans mainly spent their loan money on living expenses—with housing as the largest type of expense covered with these funds.

- Although the Post-9/11 GI Bill provides a monthly housing allowance, it often falls short of covering veterans’ actual costs. Those who reported that their housing allowance covered half or less of their housing expenses borrowed significantly more than those who reported that the housing stipend covered more than half.

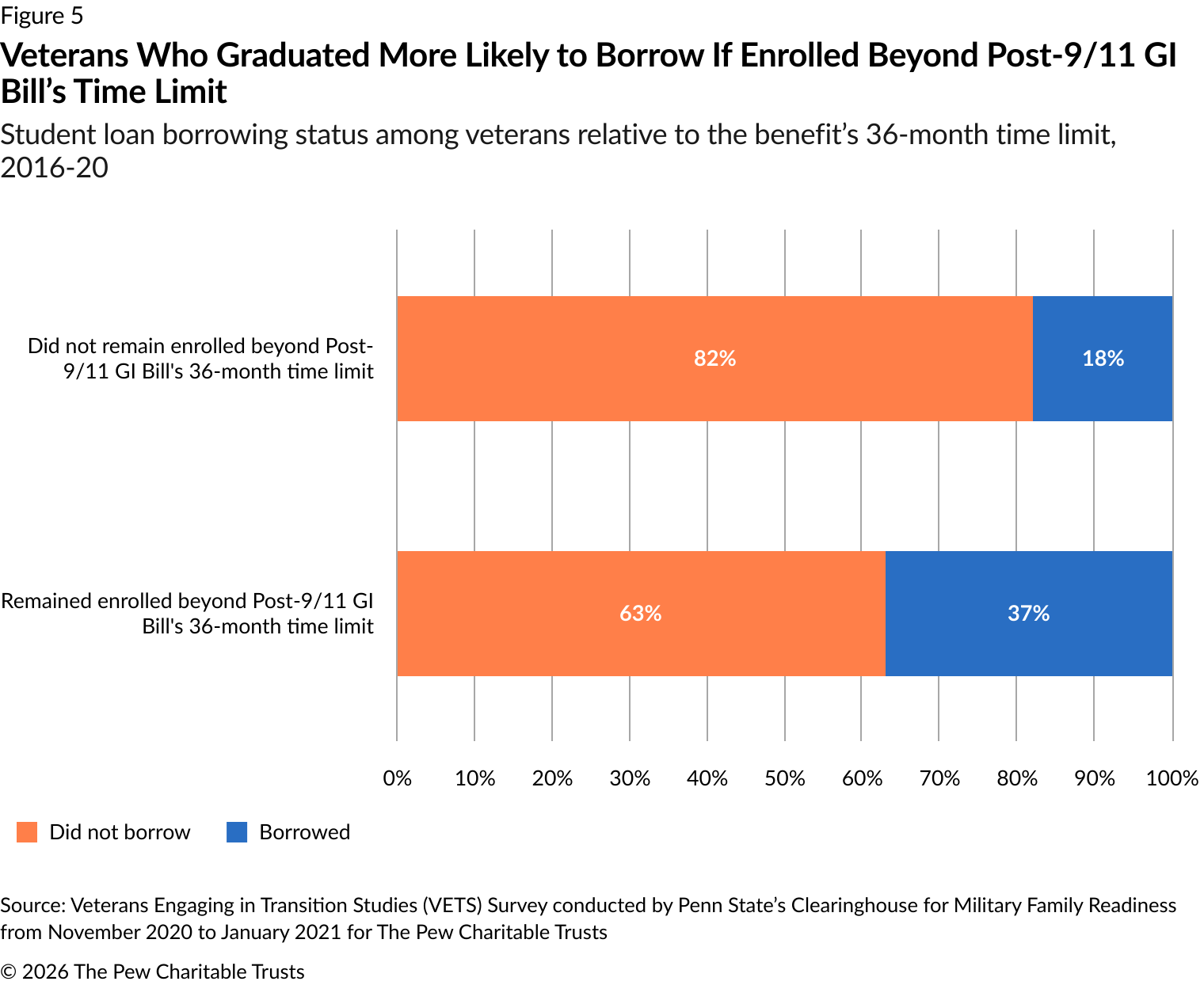

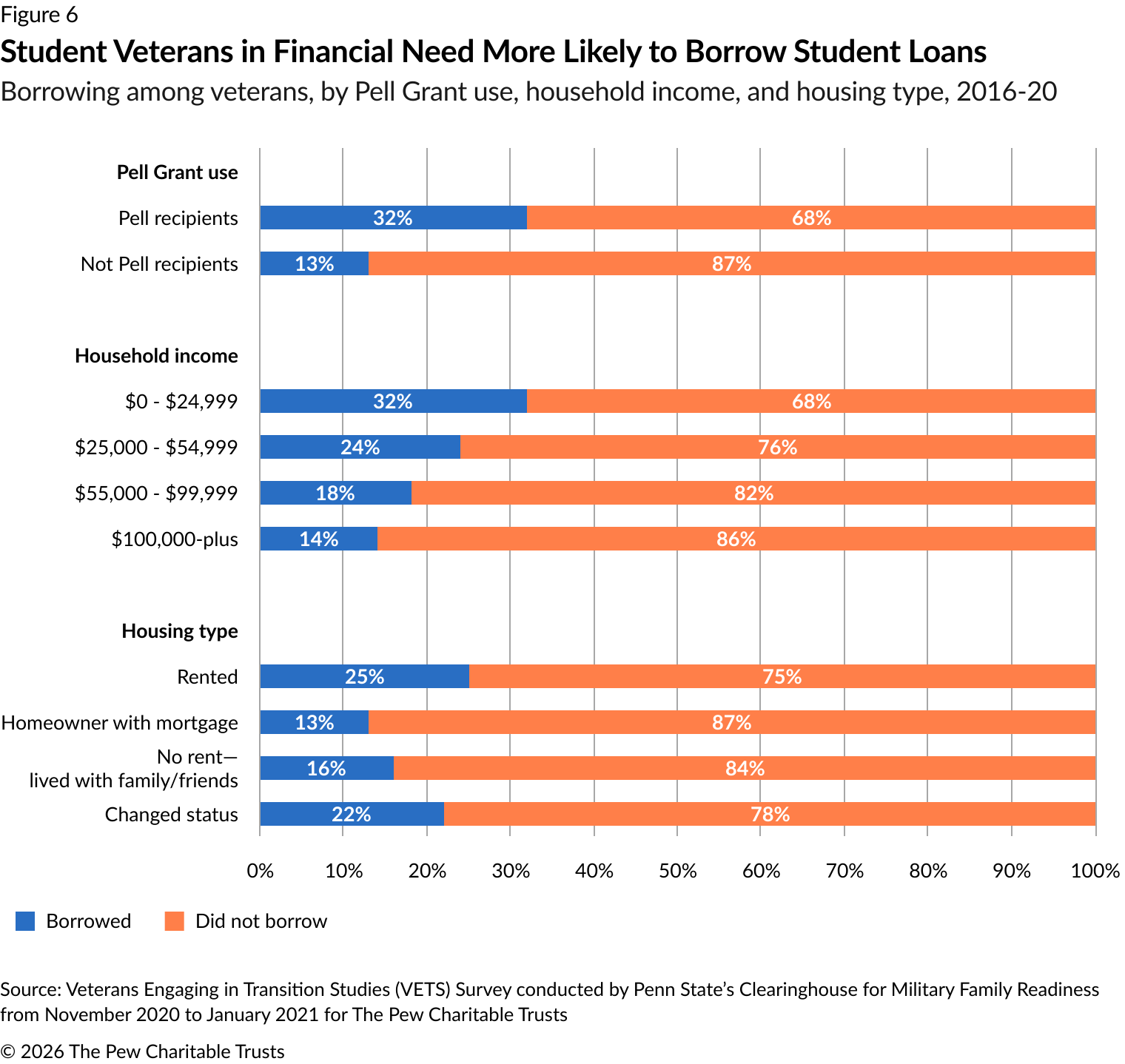

- Veterans who stayed in school beyond the Post-9/11 GI Bill’s 36-month enrollment time limit were more likely to borrow a student loan.

- Student veterans who struggled financially—as indicated by their eligibility for the Pell Grant, a need-based federal financial aid program; household income; and housing status—were more likely to take out student loans.

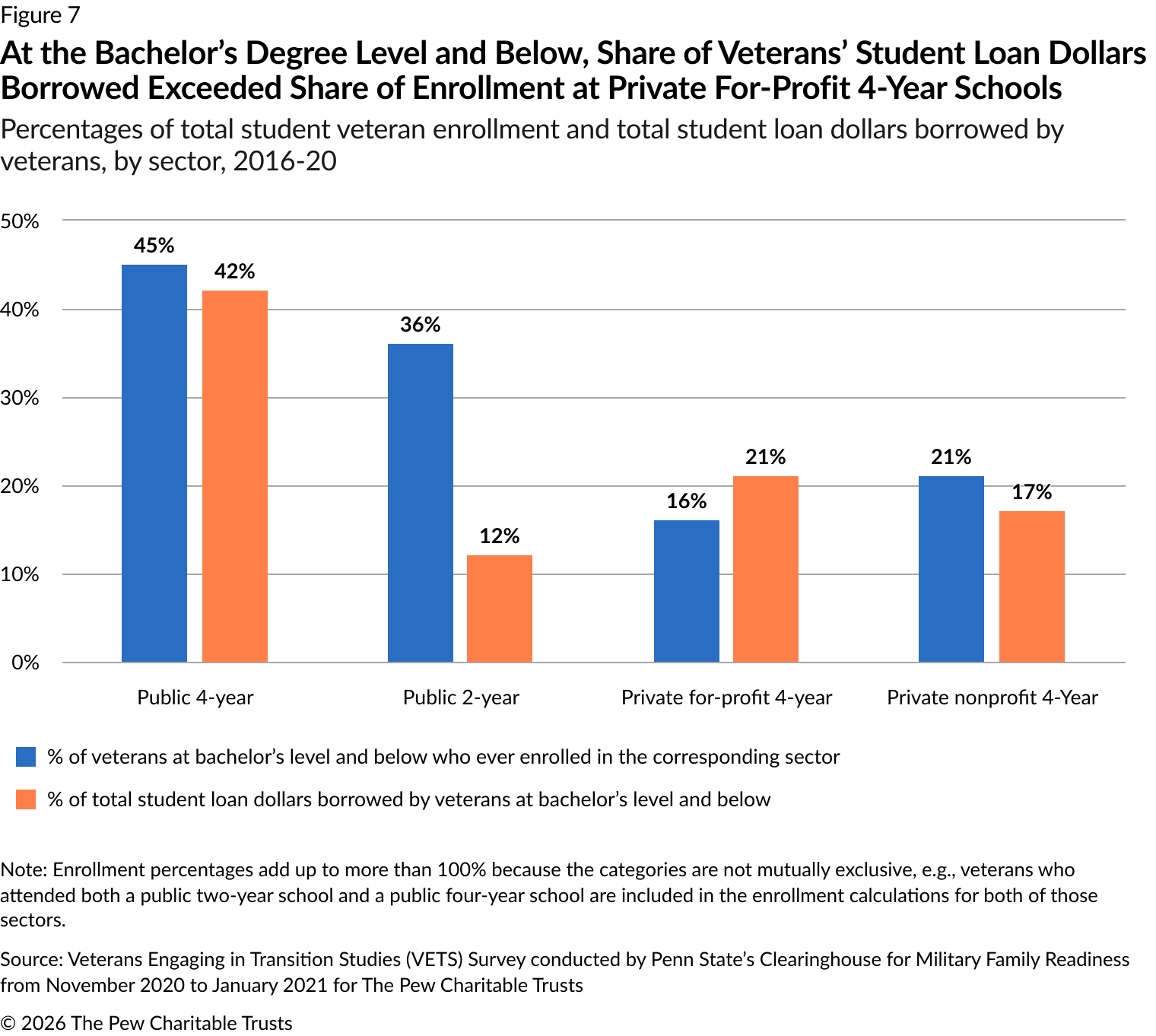

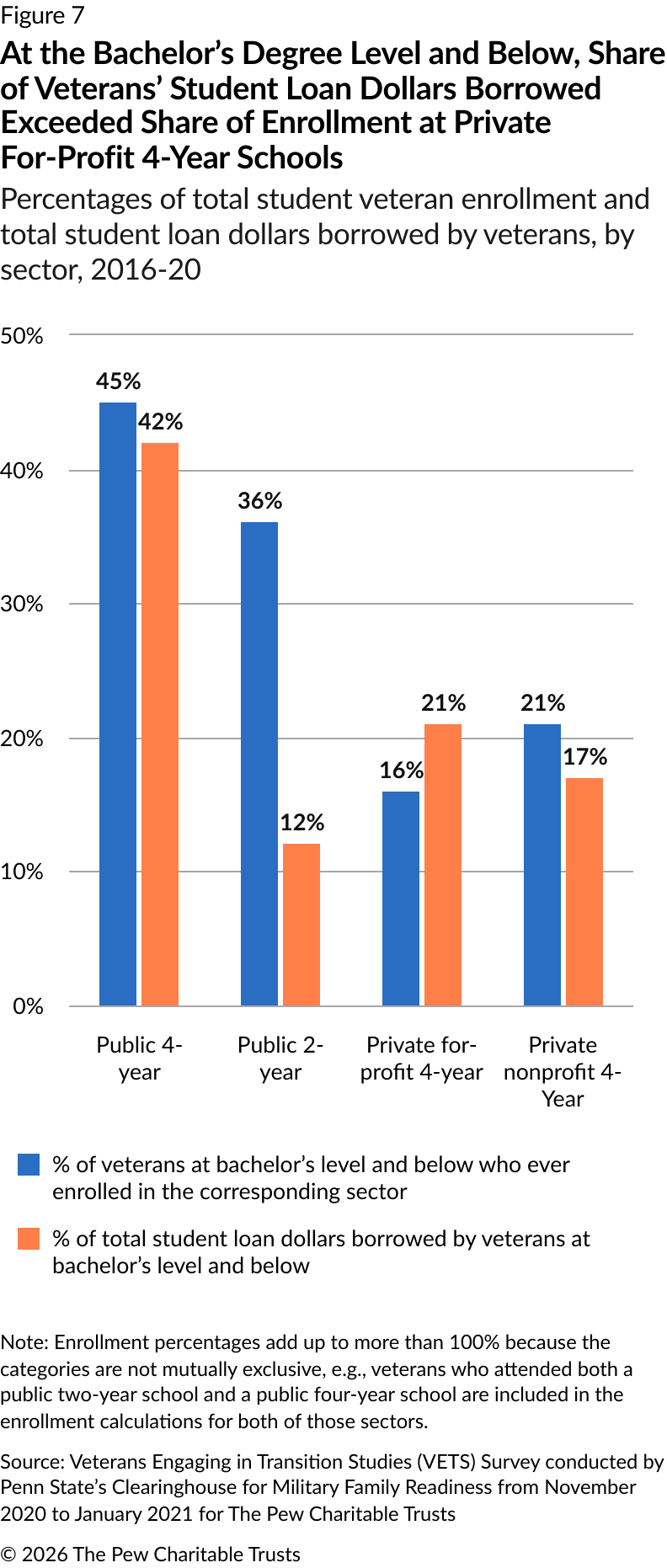

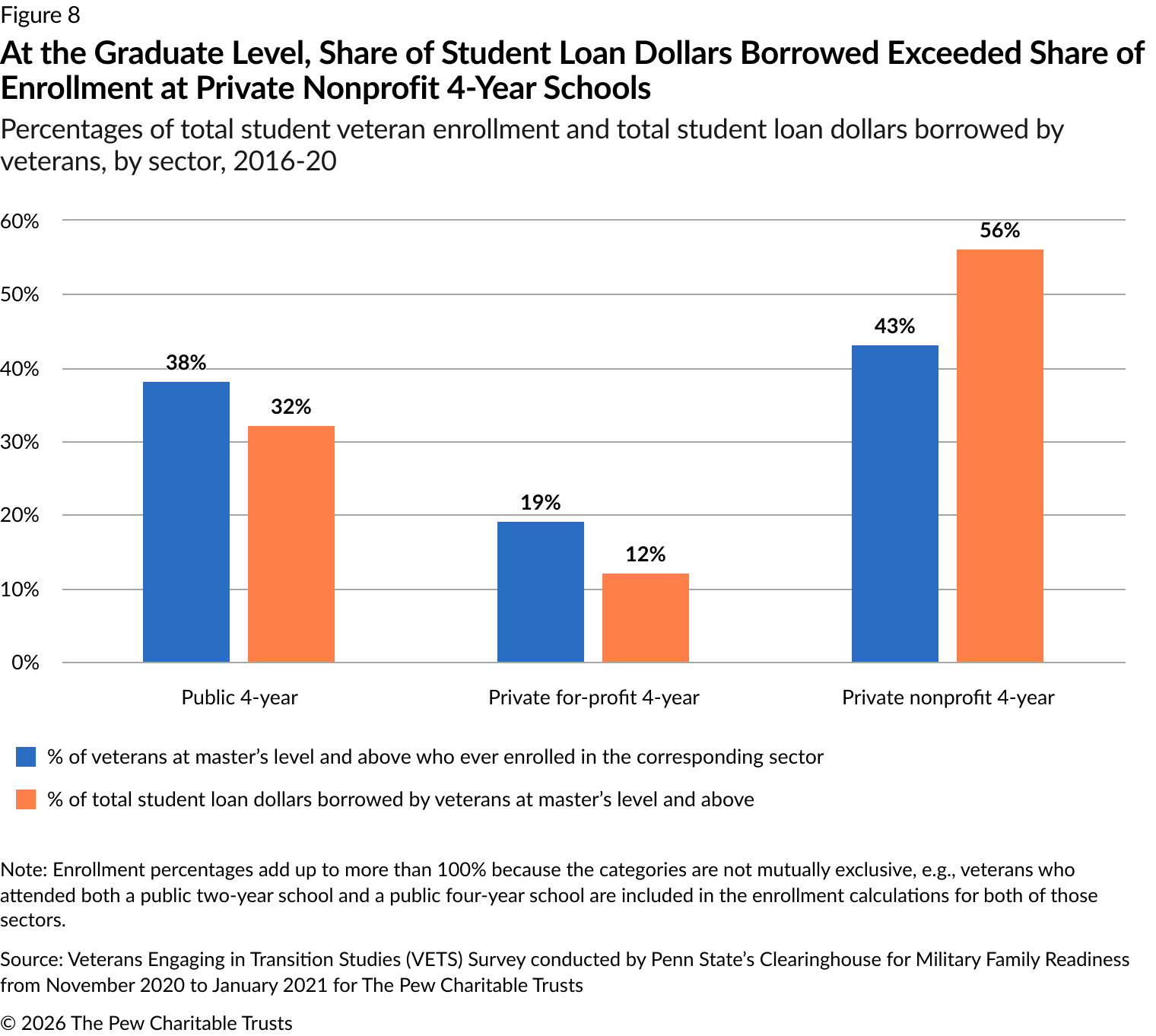

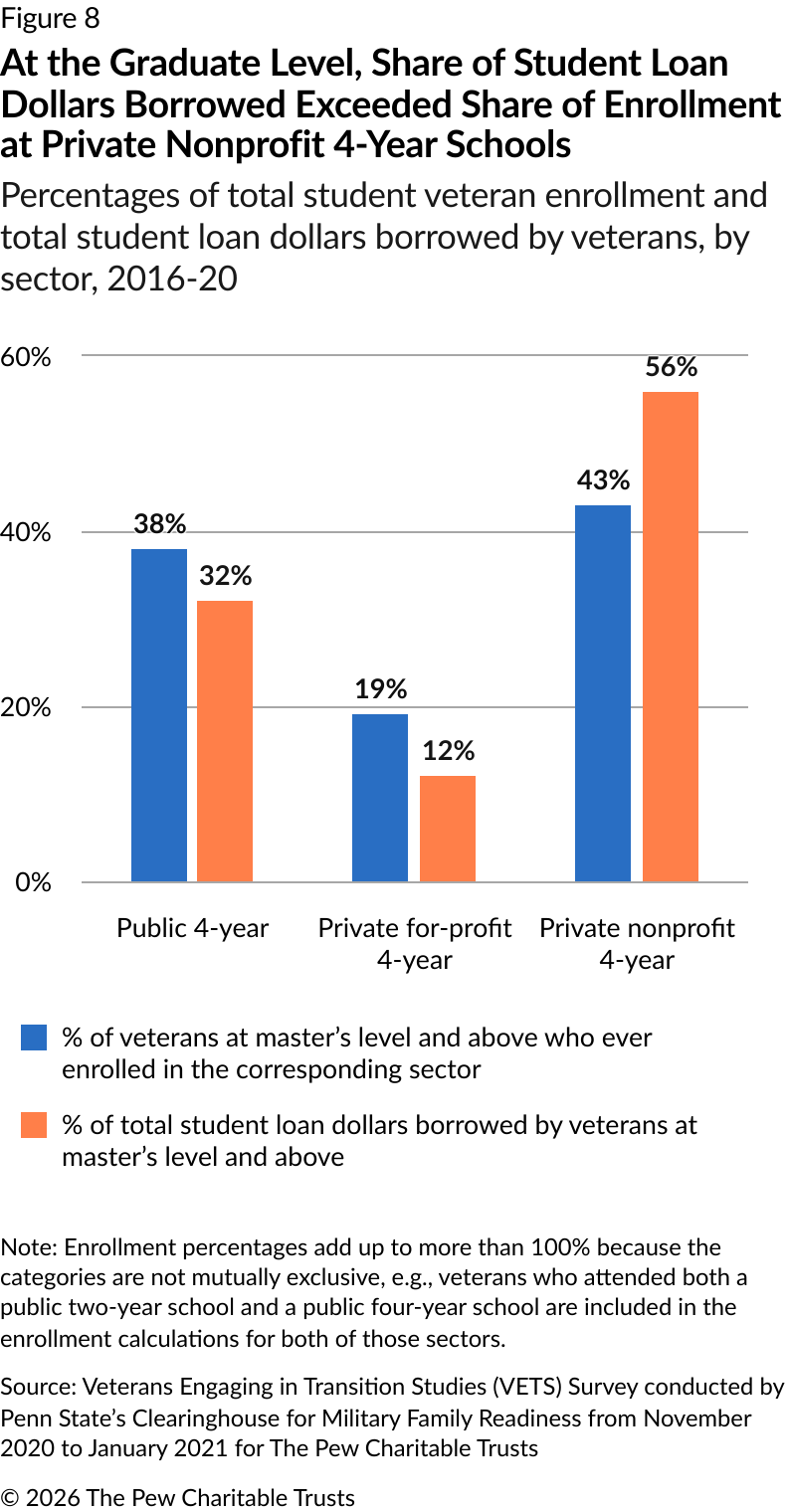

- Imbalances existed between the share of student veteran enrollment and the student loan dollars borrowed at for-profit institutions. A disproportionate share of total student loan dollars borrowed went to veterans who were enrolled at private for-profit institutions while pursuing a bachelor’s degree or below. Meanwhile, among veterans enrolled in graduate programs, the imbalance between borrowing and enrollment was greatest in the private nonprofit sector.

Pew’s survey of post-9/11 veterans gathered data about veterans’ financial circumstances over the long term to understand the broader context of veterans’ financial situations and found that 38% took on student loan debt during their lifetime. About 1 in 5 (21%) borrowed after they separated from active-duty military service—a surprisingly large share given their access to the Post-9/11 GI Bill’s robust education and training benefits.

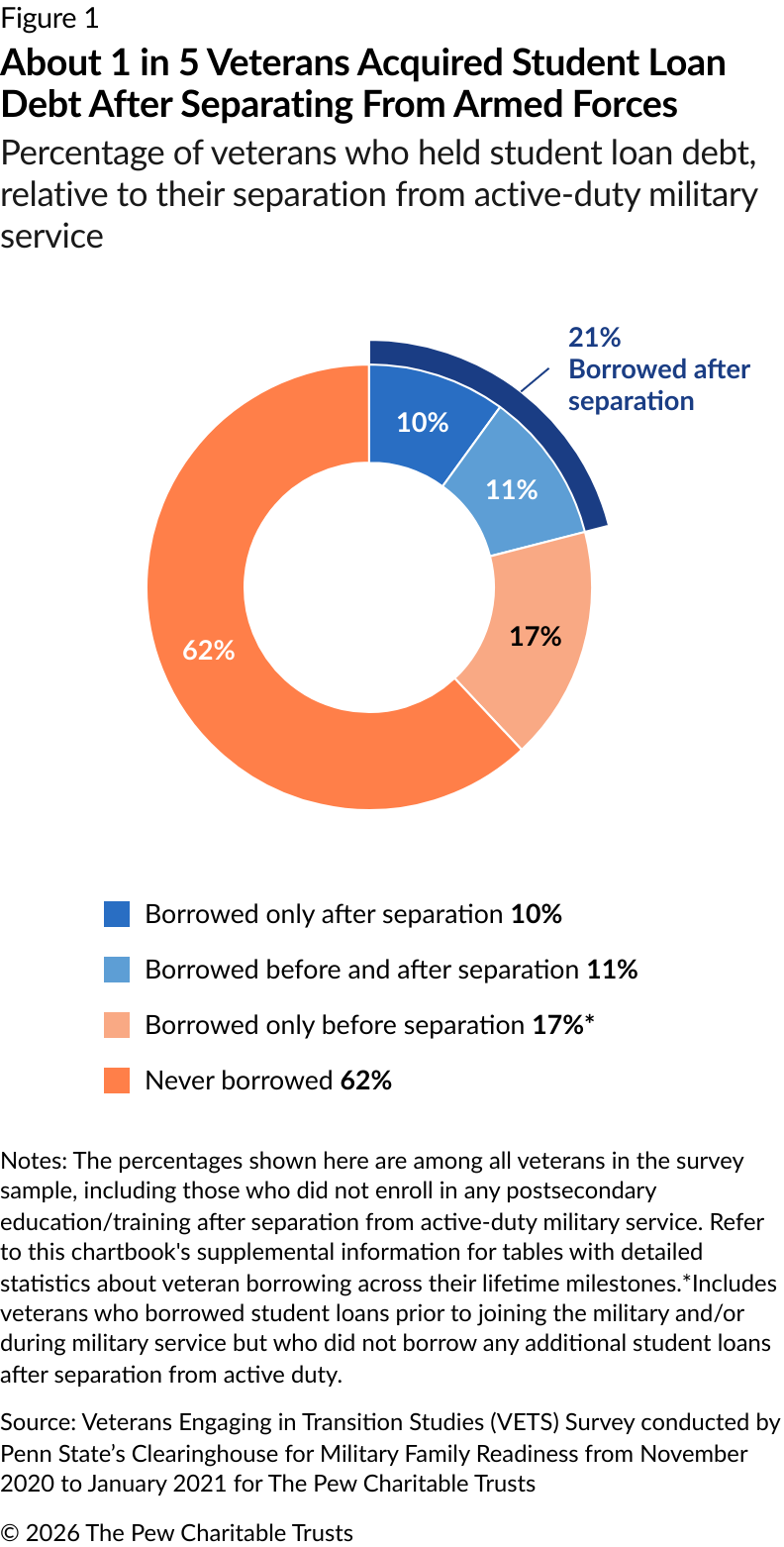

Veterans borrowed a significant amount in student loans: $22,597, on average, during an approximate four-year period after leaving the military.6 Accumulating substantial student loan debt could hamper some veterans’ military-to-civilian transitions.7 Case in point: Nearly half (46%) of student veterans who had acquired student loan debt during the first four years of their post-military transitions described their student loans as an occasional source of financial stress.8 Strikingly, 20% described the loans as a constant or overwhelming source of financial stress. Unsurprisingly, those who owed greater amounts were more likely to report higher stress levels.9

To understand how student loan stress compares with that from other forms of debt, a separate 2024 Pew survey of all student loan borrowers found that respondents who had experienced financial distress, such as struggling to keep up with debt payments, considered their student loan payments to be more stressful than other bills.10

To shed light on student veterans’ borrowing decisions, the veterans survey asked respondents about the expenses they covered using student loan funds. As shown in Figure 3, 58% of student veterans borrowed primarily to pay for living expenses, especially housing (21%), rather than for direct educational expenses such as tuition and books (42%).11

These results support research showing that living costs have become a dominant part of college expenses, especially for older students. Many of these students juggle family responsibilities, such as child care, which can add to financial pressure.12 Moreover, a Pew analysis of U.S. Department of Education data showed that student veterans are twice as likely as the general student population to have dependents.13

For many, the results depicted on the previous page in Figure 3 may be surprising, in part because the Post-9/11 GI Bill offers a monthly housing allowance designed to help eligible student veterans cover their most substantial living expense—housing—while enrolled in an approved postsecondary education or training program.14 However, the housing allowance fell short of covering actual housing costs for many veterans—and those veterans were more likely to end up with higher amounts of student loan debt.15 Figure 4 shows that the 38% of student veterans whose housing allowance covered about half or less than half of their actual housing costs borrowed an average of $25,093 during their first four years after leaving the military—an amount more than $4,000 higher than that of their peers whose allowance covered most of their housing expenses.

Veterans who stayed in school longer than the Post-9/11 GI Bill’s 36-month enrollment time limit and completed a degree or certificate at the first school they attended after separation were roughly twice as likely (37%) to take out student loans than those who finished within the limit.16 This pattern likely reflects veterans exhausting their GI Bill benefits before graduation.

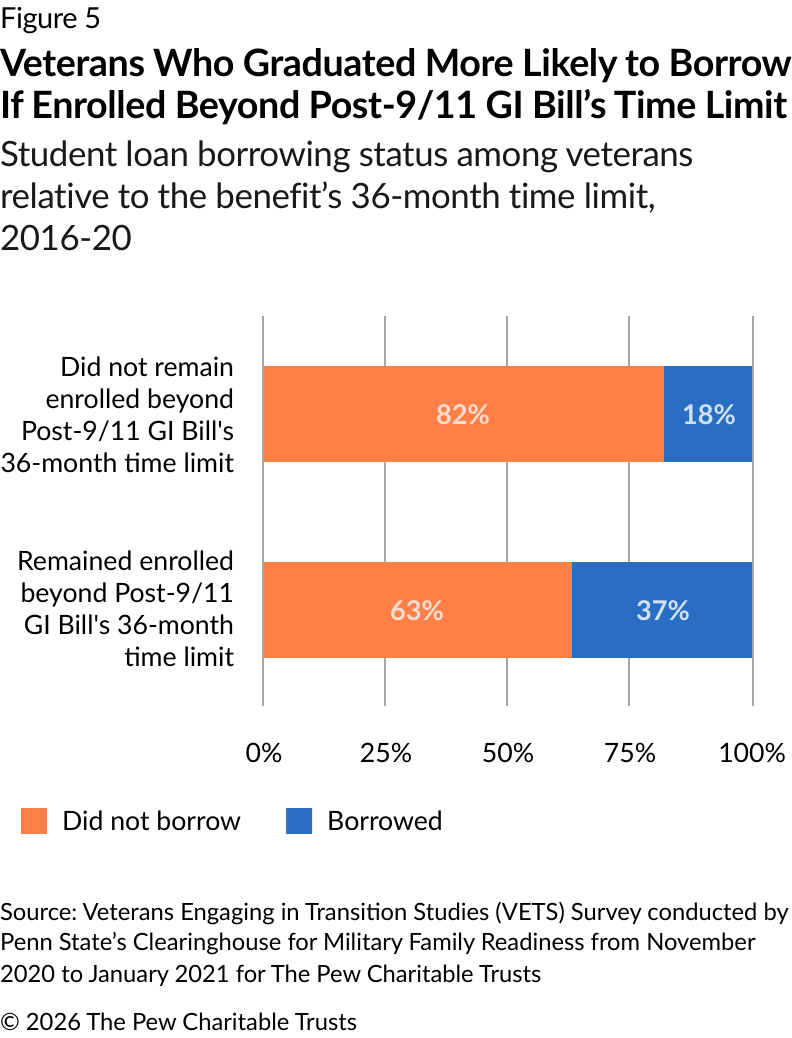

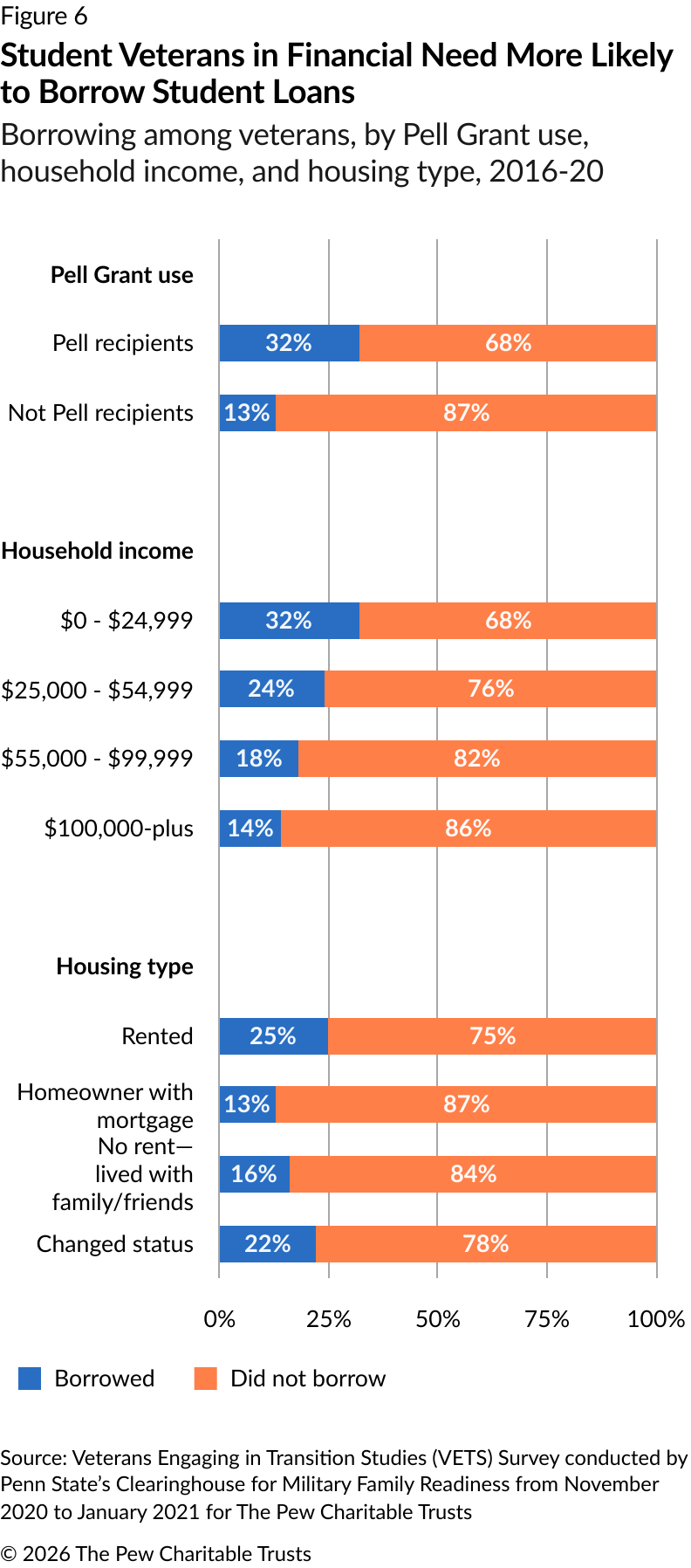

Student veterans who had the greatest financial need were the most likely to borrow student loans. One important indicator of financial need is a student’s use of federal Pell Grants to cover education costs, because the grants are typically available only to undergraduates “who display exceptional financial need.”17 Pew’s analysis shows that the percentage of student loan borrowers among student veterans who received Pell Grants (32%) was more than twice that of their peers who did not receive the grants (13%).

Two related indicators of financial need mirror this finding. First, a greater percentage of student veterans with a household income under $25,000 borrowed loans (32%) than their peers with household incomes of $100,000 or more (14%).18 Second, the share of student veteran renters who borrowed student loans (25%) was almost twice as large as that of their peers who were homeowners (13%). Renters typically have lower levels of household wealth than homeowners. In fact, according to the Aspen Institute, the median wealth gap between the two groups in 2022 was about $386,000, highlighting how renters often have far less financial cushion than homeowners, which may contribute to higher student loan borrowing.19

Survey analysis revealed a link between the type of school that veterans attended and their student loan borrowing.20 Among veterans enrolled in bachelor’s degree programs and below, the share of total student loan dollars borrowed exceeded the share of student veteran enrollment in just one sector: private for-profit four-year institutions. In this sector, 21% of all student loan dollars were borrowed by veterans even though the share of total veteran enrollment was just 16%.21

Although many factors may contribute to the disproportionate share of borrowing observed among student veterans at private for-profit institutions, the following are particularly relevant in regard to the Post-9/11 GI Bill:

- Tuition and fees at many private for-profit schools exceed the Post-9/11 GI Bill’s annual maximum of $29,921.22 Some—but not all—private institutions participate in the Yellow Ribbon Program to help veterans bridge the gap between tuition costs and benefits.23

- Many schools that were among the top recipients of Post-9/11 GI Bill funds during fiscal years 2009-17 were for-profit colleges and universities that mainly offered online programs of study.24 Veterans enrolled in purely online programs receive a reduced housing allowance—and a prior Pew analysis showed that veterans in these programs were more likely to report that their housing stipend fell short of actual housing costs than their peers who took some portion of their courses in person.25

In contrast, public four-year institutions accounted for the largest number of student veterans enrolled, so they naturally received the largest total share of loan dollars. However, the mismatch between housing costs and the Post-9/11 GI Bill’s monthly housing allowance (as noted in Figure 4) affects student veterans in every sector, including those attending public schools.

For those enrolled in programs at the master’s level and above, private nonprofit four-year institutions were the most popular among student veterans. This sector also had a disproportionately high share of total loan dollars relative to enrollment: 56% of loan dollars went to veterans enrolled there, even though only 43% of graduate student veterans attended. Notably, this was the only sector at any study level accounting for more than half of all loan dollars.

The borrowing patterns observed among veterans attending programs at this level may shift soon. The federal tax and spending bill passed in July 2025 will phase out the Grad PLUS loan program in 2026. These loans allowed eligible students in graduate and professional degree programs to borrow any amount needed to cover the total cost of attendance.26 However, the end of Grad PLUS will be coupled with new borrowing limits. Federal student loans will be capped at $100,000 total for graduate degree programs and $200,000 total for professional degree programs.27

Endnotes

- "Post-9/11 GI Bill (Chapter 33) Rates," U.S. Department of Veterans Affairs, Aug. 1, 2025, https://www.va.gov/education/benefit-rates/post-9-11-gi-bill-rates. Some private institutions participate in the Yellow Ribbon Program, which covers some or all of the gap between the maximum Post-9/11 GI Bill tuition/fee level and their actual tuition and fees. See: U.S. Department of Veterans Affairs, "Yellow Ribbon Program," accessed Aug. 4, 2022, https://www.va.gov/education/about-gi-bill-benefits/post-9-11/yellow-ribbon-program/.

- U.S. Department of Veterans Affairs, "Benefits for Veterans Education," U.S. Department of Veterans Affairs, 2024, https://www.benefits.va.gov/REPORTS/abr/docs/2024-education.pdf.

- Phillip Oliff et al., "Veteran Student Loan Debt Draws New Attention," The Pew Charitable Trusts, Sept. 13, 2021, https://www.pewtrusts.org/en/research-and-analysis/articles/2021/09/13/veteran-student-loan-debt-draws-new-attention.

- This finding is based on Pew's analysis of the Veterans Engaging in Transition Studies (VETS) Survey, which is a nationally representative survey of post-9/11 veterans conducted by Penn State in late 2020 to early 2021 on behalf of The Pew Charitable Trusts. All survey respondents separated from active-duty military service in 2016, and the survey was designed to capture data about their transition from military to civilian life over a four-year period. For more details, refer to the methodology and toplines of Penn State's VETS Survey, which are available as downloadable supplements to this chartbook. The average borrowing statistic shown here includes all veterans in the VETS Survey sample who had borrowed a federal student loan for any level of study following their separation from active-duty military service. Comparable data about student loan debt among nonveterans during this same time frame (2016-20) is not available.

- A variety of stakeholders focused on supporting student veterans asked Pew to determine if veterans who used the Post-9/11 GI Bill were less likely to borrow student loans or if they borrowed less. Despite its robust benefits, the correlation between veterans' GI Bill use and their student loan borrowing status was not statistically significant. Likewise, there was no statistically significant correlation between student loan borrowing status and the following demographics/characteristics: gender, age, race/ethnicity, community category (metro or nonmetro), employment while enrolled, prior rank in the military, family status while enrolled, learning mode (e.g., online vs. in-person/hybrid), and rate of pursuit (i.e., enrolled full time vs. part time). As shown in Table 3B of the supplement that accompanies this chartbook, the median amount borrowed among all student veterans who took out one or more student loans during 2016-20 was $15,000, whereas the median amount borrowed among those who used Post-9/11 GI Bill benefits and borrowed student loans during that same time frame was $14,500. Due to sample size limitations, a precise estimate of the median amount borrowed is not available for those who borrowed student loans but did not use Post-9/11 GI Bill benefits.

- According to Bullington et al.'s 2024 analysis of the Department of Education's Baccalaureate and Beyond Longitudinal Study, the average amount of student loan debt held by student veterans who had earned an undergraduate degree in 2016 was $17,478. Note that the findings shown in Figure 2 include graduate and undergraduate student veterans in Penn State's VETS Survey, whereas the Baccalaureate and Beyond Longitudinal Study covered only undergraduates. Kim E. Bullington et al., "Is the GI Bill Enough? An Exploratory Analysis of Student Veteran Borrowing in College," Universal Journal of Financial Economics, 2024, https://digitalcommons.odu.edu/cgi/viewcontent.cgi?article=1143&context=efl_fac_pubs.

- Karre et al. rated veterans' military-to-civilian transitions across seven domains as successful, at-risk, or problematic. Alarmingly, less than half (48%) attained a "successful" rating in the financial domain at the 2.5-year mark after separation from the military. However, more research is needed to determine the extent to which debt accumulation in general—and student loan debt in particular—are associated with transition outcomes in the financial domain and in other domains. J. K. Karre et al., "What Do Successful Military-to-Civilian Transitions Look Like? A Revised Framework and a New Conceptual Model for Assessing Veteran Well-Being," Armed Forces & Society, Sage Journals, 2024, https://doi.org/10.1177/0095327X231216678.

- This percentage does not include veterans who acquired student loan debt after separation from active-duty military service in 2016 and paid off those loans prior to the survey (late 2020).

- Twenty-nine percent of veterans who had borrowed $25,000 or more in student loans after separation reported feeling constant or overwhelming levels of stress, whereas 16% of veterans who borrowed less than $25,000 reported similar levels of stress.

- Richa Bhattarai, Lexi West, and Janette Barbosa, "For Many Student Loan Borrowers, Financial Security Feels out of Reach," The Pew Charitable Trusts, 2025, https://www.pew.org/en/research-and-analysis/issue-briefs/2025/06/for-many-student-loan-borrowers-financial-security-feels-out-of-reach.

- The following subpopulations of student veterans were overrepresented among those who mainly used their loan funds for living expenses: undergraduates, full-time students, Pell Grant recipients, and prior enlisted veterans. Please refer to the tables in this chartbook's supplement for more details about use of student loan funds among these subgroups.

- Vincent Palacios et al., "Obstacles to Opportunity: Increasing College Success by Understanding & Addressing Older Students' Costs Beyond Tuition," Center on Poverty and Inequality, Georgetown University, 2021, https://www.georgetownpoverty.org/wp-content/uploads/2021/05/CBT-Obstacles-to-Opportunity-Report-May2021.pdf.

- Phillip Oliff, Scott Brees, and Richa Bhattarai, "Why Veterans With GI Bill Benefits Still Take Out Student Loans," The Pew Charitable Trusts, 2022, https://www.pew.org/en/research-and-analysis/articles/2022/01/07/why-veterans-with-gi-bill-benefits-still-take-out-student-loans.

- "Post-9/11 GI Bill (Chapter 33) Rates," U.S. Department of Veterans Affairs.

- The housing allowance a student veteran is eligible to receive can vary greatly, depending on a variety of factors, such as the student's level of eligibility for Post-9/11 GI Bill benefits, mode of enrollment (online vs. in-person), course load (full time vs. part time), and campus location. Furthermore, the housing allowance is not disbursed during school breaks, among other important limitations. For more details, refer to: Phillip Oliff et al., "A Primer on the Post-9/11 GI Bill's Monthly Housing Allowance," The Pew Charitable Trusts, 2025, https://www.pew.org/-/media/assets/2025/11/virtualclassroom_supplemental1_issuebrief_2025_final.pdf.

- The Post-9/11 GI Bill's 36-month time limit equates to four traditional academic years, with approximately nine months of time in class and three months of breaks per calendar year. The Department of Education considers four years to be the normal time needed to complete a bachelor's degree. "Graduation Rates (GR)," National Center for Education Statistics, Department of Education, https://nces.ed.gov/ipeds/survey-components/9. However, veterans with two or more qualifying periods of active-duty service may claim up to 48 months of benefits by combining Post-9/11 GI Bill benefits with Montgomery GI Bill benefits. "Post-9/11 GI Bill (Chapter 33)," U.S. Department of Veterans Affairs, Aug. 3, 2022, https://www.va.gov/education/about-gi-bill-benefits/post-9-11. Furthermore, veterans with a service-connected disability rating of at least 10% from the VA may use Veteran Readiness & Employment benefits to cover education and training costs for up to 48 months without deducting from their Post-9/11 GI Bill or Montgomery GI Bill benefits. See: "Eligibility for Veteran Readiness and Employment," U.S. Department of Veterans Affairs, Nov. 7, 2025, https://www.va.gov/careers-employment/vocational-rehabilitation/eligibility/.

- The Free Application for Federal Student Aid (FAFSA) form is used to collect students' financial data, such as income, savings, and investments. This data is used to generate a Student Aid Index (SAI), which in turn determines eligibility for the Pell Grant and other forms of financial aid. "How Is the Student Aid Index (SAI) Calculated?," Federal Student Aid, https://studentaid.gov/help-center/answers/article/how-sai-calculated. Federal Student Aid. "Federal Pell Grants." U.S. Department of Education.

- The household income figures shown are as of the date of the survey (November 2020 to January 2021, approximately four years after separation from respondents' active-duty military service).

- Shehryar Nabi and Steven Brown, "From Rent to Riches? A Profile on the Wealth and Financial Well-Being of Renter Households," 2024, https://www.aspeninstitute.org/publications/from-rent-to-riches-a-profile-on-renter-wealth/. As shown on Figure 1, p. 5, the median net worth of homeowners was $396,500 vs. $10,400 among renters in 2022.

- The following sectors are not shown in Figure 8: private nonprofit two-year, private for-profit two-year, public less-than-two-year, private for-profit less-than-two-year, Department of Defense-funded institutions, and other private and public institutions that offer shorter training and certification programs. Altogether, these sectors accounted for 12% of enrollment at the bachelor's degree level and below.

- Similarly, Bullington et al. found that student veterans who had earned an undergraduate degree from a private institution borrowed an average of $4,661 more than their peers who graduated from public colleges. Kim E. Bullington et al., "Is the GI Bill Enough? An Exploratory Analysis of Student Veteran Borrowing in College."

- "Post-9/11 GI Bill (Chapter 33) Rates," U.S. Department of Veterans Affairs.

- U.S. Department of Veterans Affairs, "Yellow Ribbon Program."

- Walter Ochinko and Kathy Payea, "Schools Receiving the Most Post-9/11 GI Bill Tuition and Fee Payments Since 2009," Veterans Education Success, 2018, https://vetsedsuccess.org/schools-receiving-the-most-post-9-11-gi-bill-tuition-and-fee-payments-since-2009/. According to enrollment data available from the National Center for Education Statistics, the following for-profit institutions listed in the VES report offered most or all of their course content online: University of Phoenix, DeVry University, Career Education Corporation (now Perdoceo Education Corporation, which owns/operates Colorado Technical University and the American Intercontinental University System), and Strayer Education Inc. "College Navigator," National Center for Education Statistics, Department of Education, https://nces.ed.gov/collegenavigator/.

- See Figure 2 of Phillip Oliff et al., "Monthly Housing Allowance Basics: From Big Cities to Small Towns."

- "Direct Plus Loans for Graduate or Professional Students," Federal Student Aid, https://studentaid.gov/understand-aid/types/loans/plus/grad.

- The Grad PLUS program's termination applies to students seeking new federal student loans after July 1, 2026. Those enrolled in a graduate program prior to 2026 who have up to three years remaining in their program of study may continue to participate in the Grad PLUS program. Ben Unglesbee, "What Does the End of Grad Plus Loans Mean for Higher Ed?," Higher Ed Dive, Sept. 22, 2025, https://www.highereddive.com/news/end-of-grad-plus-loans-impact-higher-ed/760448/.

People