Indiana Residents Often Use Land Contracts to Purchase Low-Cost Homes

Thousands of Indiana buyers have turned to risky mortgage alternatives in the past 20 years

Overview

Tens of thousands of Indiana residents have used land contracts to purchase homes, farms, and other properties over the last two decades. Land contracts—sometimes referred to as “contracts for deed” or “land installment contracts”—are often risky and costly for buyers. But individuals who are unable to obtain a mortgage, are seeking to purchase homes that are difficult to finance through traditional channels, or are shut out from the mainstream financial system often turn to land contracts when they lack safer options.

This fact sheet provides an overview of Indiana's land contract market. Researchers from The Pew Charitable Trusts analyzed county-level property transaction records in Indiana from 2005 to 2024 to identify geographic regions where land contracts are most common, the size and age of homes purchased with land contracts, and how land contract use varies across different housing markets.

What is a land contract?

A land contract is a form of alternative financing in which a buyer purchases a home or other piece of real estate directly from the seller rather than through a mortgage lender. Typically, the buyer makes a down payment to the seller, who finances the remaining balance of the purchase price. The buyer makes installment payments over time at a specified interest rate until the contract is fully repaid.

Unlike mortgage borrowers, land contract buyers do not receive legal title to the property until the final payment is made. As a result, buyers assume many of the responsibilities of homeownership—such as maintenance, repairs, and property taxes—without the same legal protections and tax advantages enjoyed by mortgage borrowers. Pew’s prior research shows that in some jurisdictions, land contract buyers who miss payments can be removed from their homes more quickly than mortgage borrowers, because courts treat land contracts more like rental agreements than traditional homeownership.1 Without access to the foreclosure process, land contract buyers risk losing all their equity in a home, even if they have been making payments for years.

In Indiana, one recent analysis found that land contracts recorded in Marion County (which includes Indianapolis) from 2018 to 2023 were concentrated in low- and moderate-income neighborhoods and appeared to be marketed to the capital's Hispanic communities.2 That research also found that land contracts are sometimes used to finance distressed or substandard properties, which puts the onus of home repairs on buyers, even though they do not have full ownership rights to the property.

Facts about Indiana’s land contract market

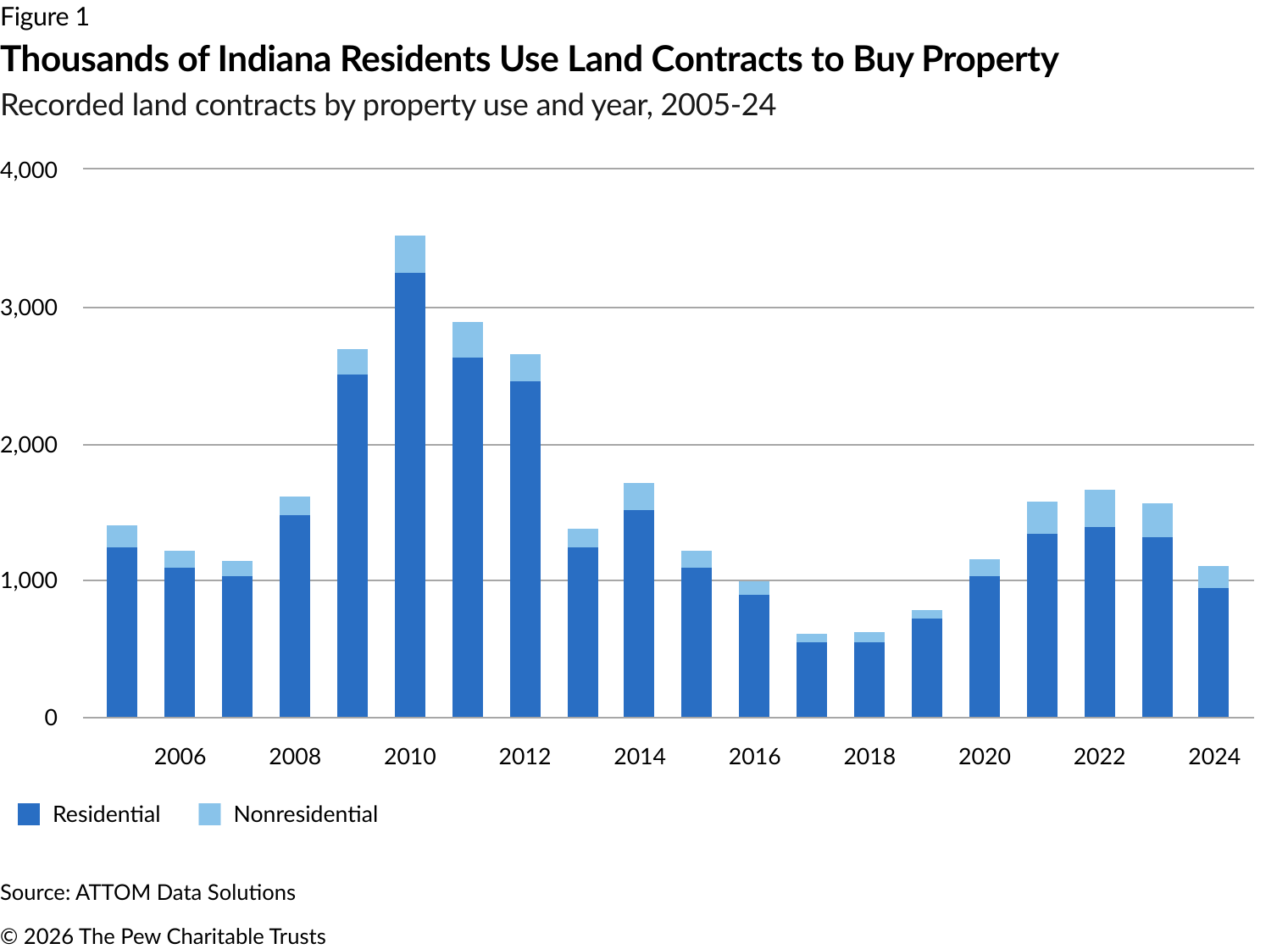

Land contracts are common in Indiana. From 2005 to 2024, county governments in Indiana recorded 31,431 land contracts—the sixth most land contracts of any state, even though Indiana ranked 17th in population in 2024. Of those contracts, 28,192 (90%) were used to acquire residential properties, while the remainder financed businesses, farms, or vacant land. (See Figure 1.) The number of recorded land contracts in Indiana peaked at 3,521 in 2010 and declined to a low of 612 in 2017. Indiana counties recorded 1,098 land contracts in 2024.

Buyers often use land contracts to acquire low-cost homes. In Indiana, an estimated 332,600 homes sold for less than $150,000 between 2005 and 2024 (inflation-adjusted to 2024 dollars). About 4.2% of these homes were purchased with a land contract, while 24.4% were purchased with a mortgage. (Most of the remaining homes were purchased with cash.) The numbers look very different for higher-cost homes. Of the roughly 619,000 homes that sold for more than $150,000 during the study period, just 1.5% were financed with a land contract. Nearly two-thirds (65.6%) were financed with a mortgage.

Pew’s research has shown that it can be difficult for buyers nationwide to get mortgages for homes under $150,000.3 When small mortgages are unavailable, some homebuyers turn to alternative financing arrangements—including land contracts—to finance their purchase.

Overall, the inflation-adjusted median sales price of a home in Indiana financed with a land contract was $122,313—substantially lower than the $207,512 statewide median sales price for all home purchases.

Manufactured home buyers use land contracts more frequently than buyers of traditional houses. Manufactured homes are one of the most affordable housing types in Indiana, with an inflation-adjusted median sales price of $106,523 (in 2024 dollars). However, Pew’s research has shown that applicants for loans on manufactured homes are five-to-nine times more likely to be denied credit than prospective buyers of traditional site-built homes.4 Some individuals who cannot get a traditional loan turn to land contracts.

County records show that 37,544 manufactured homes were sold as real estate in Indiana between 2005 and 2024. (In Indiana, as in most other states, many manufactured homes are titled and sold as personal property instead of real estate, making them ineligible for financing with a mortgage.) Among manufactured home buyers, an estimated 3.2% (1,215) used a land contract—a percentage that is substantially higher than the 1.2% of buyers of traditional site-built homes who used land contracts.

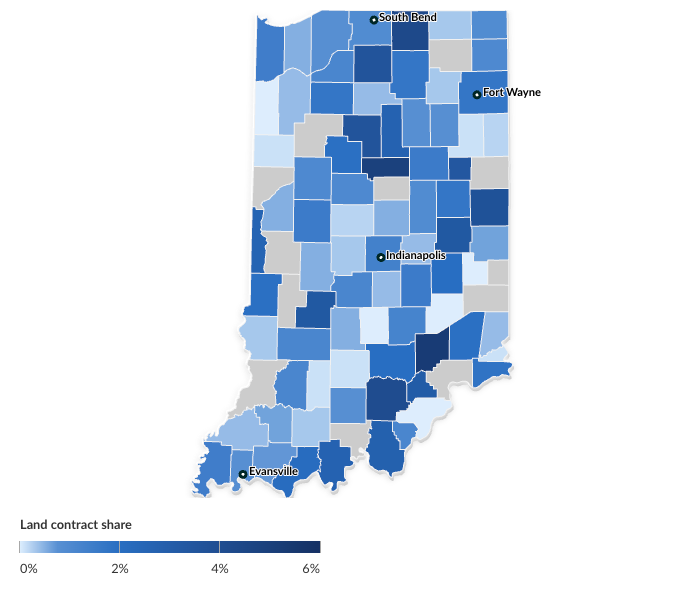

As a result, counties with a high concentration of manufactured homes tended to have a higher incidence of land contract utilization. For example, Indiana’s Jennings County and Washington County each had some of the state’s highest number of manufactured home sales during the 20-year study period; both also had high percentages of land contracts as a share of total home sales. (See Figure 2.)

Land contracts are common in both urban and rural areas of Indiana. Large numbers of land contracts were recorded in Marion County (which contains Indianapolis), Allen County (which contains Fort Wayne), and Lake County (which contains parts of suburban Chicago). However, about 22% of all residential land contracts were recorded outside Indiana’s metropolitan areas, even though these rural areas accounted for just 16% of the state’s home sales.

Land contracts are more often used to finance smaller, older homes. The median construction year of a home purchased with a land contract in Indiana during the study period was 1952—18 years older than the median for all homes sold in the state. And the median size of a home purchased with a land contract was just 1,480 square feet, compared with a median of 1,776 square feet for all homes sold in Indiana during the same period.

Land contract sellers are often corporate entities. A significant minority of land contract sellers (30%) in Indiana were corporate entities—a rate similar to that of corporate sellers involved in all home sales statewide (32%). However, corporate sellers were more common in Marion County, where nearly half of all land contracts involved companies. Corporate buyers were less common, making up just 8% of land contract buyers and 18% of all homebuyers statewide.

Land contracts are more expensive than mortgages. From 2005 to 2024, land contracts carried a median interest rate of 7%, compared with a 6.1% median rate for mortgages. However, land contract down payments were smaller: 4.8% of the total sales price, compared with 7.4% for mortgage-financed home sales. For some land contract buyers, the relatively small down payment is part of the appeal.

Facts about Indiana’s land contract laws

Indiana does not have a comprehensive state law regulating land contracts. Land contracts in Indiana are addressed piecemeal through several state laws, including the First Lien Mortgage Lending Act and the Home Loan Practices Act, and one key state supreme court Supreme Court decision.5 No single law clearly and comprehensively addresses the risks and challenges associated with land contracts in Indiana.

Indiana law provides limited legal protections to land contract buyers. Under Indiana law, sellers are required to disclose any encumbrances affecting the home’s title (such as tax liens, foreclosure actions, legal judgments, or other claims) within the first 10 days of the contract. Sellers are also forbidden to charge a fee to buyers who prepay their contracts. However, there is no requirement that sellers publicly record land contracts with local governments, nor are there restrictions on a land contract’s interest rate, fees, or contract terms.

The Indiana Supreme Court has ruled that land contracts should be treated like mortgages. A 1973 Indiana Supreme Court case established that a land contract in the state should in certain cases be treated like a mortgage rather than a typical sales contract, in which the buyer would forfeit all equity upon cancellation for nonpayment.6 This ruling enables some land contract buyers in Indiana to go through the foreclosure process, which typically gives them more time to catch up on missed payments and allows them to retain their home equity, rather than a quicker and less borrower-friendly forfeiture process. However, there is no law codifying this distinction; in Marion County, many recorded land contracts contain provisions that limit foreclosure to buyers who have paid off at least a minimum amount of the contract (typically between 15% and 60% of the balance).7

Endnotes

- Adam Staveski, Linlin Liang, and Tara Roche, “Land Contracts Pose 5 Major Risks for Homebuyers,” The Pew Charitable Trusts, 2024, https://www.pew.org/en/research-and-analysis/issue-briefs/2024/07/land-contracts-pose-5-major-risks-for-homebuyers.

- “The State of Fair Housing in Indiana Report—Land Contracts: The Promise and Perils of Alternative Home Financing,” Fair Housing Center of Central Indiana, 2024, https://www.fhcci.org/wp-content/uploads/2024/07/Land-Contract-Report-FINAL-6-30-24.pdf.

- The Pew Charitable Trusts, “Small Mortgages Are Too Hard to Get,” 2023, https://www.pew.org/en/research-and-analysis/issue-briefs/2023/06/small-mortgages-are-too-hard-to-get.

- “Data Shows Lack of Manufactured Home Financing Shuts Out Many Prospective Buyers,” Linlin Liang, Rachel Siegel, and Adam Staveski, The Pew Charitable Trusts, Dec. 7, 2022, https://www.pew.org/en/research-and-analysis/articles/2022/12/07/data-shows-lack-of-manufactured-home-financing-shuts-out-many-prospective-buyers.

- Indiana Code, § 24-9, 2025, https://law.justia.com/codes/indiana/title-24/article-9/. Indiana Code, § 24-4.4, 2025, https://law.justia.com/codes/indiana/title-24/article-4-4/. Skendzel v. Marshall, 301 N.E.2d 641 (Ind. 1973), https://law.justia.com/cases/indiana/supreme-court/1973/773s145-2-0.html.

- Skendzel v. Marshall, 301 N.E.2d 641.

- The Pew Charitable Trusts, “The State of Fair Housing in Indiana Report.”

People