States Are Leveraging Financing Institutions to Strengthen Infrastructure

Independent authorities help communities plan, pay for, and manage long-term capital needs

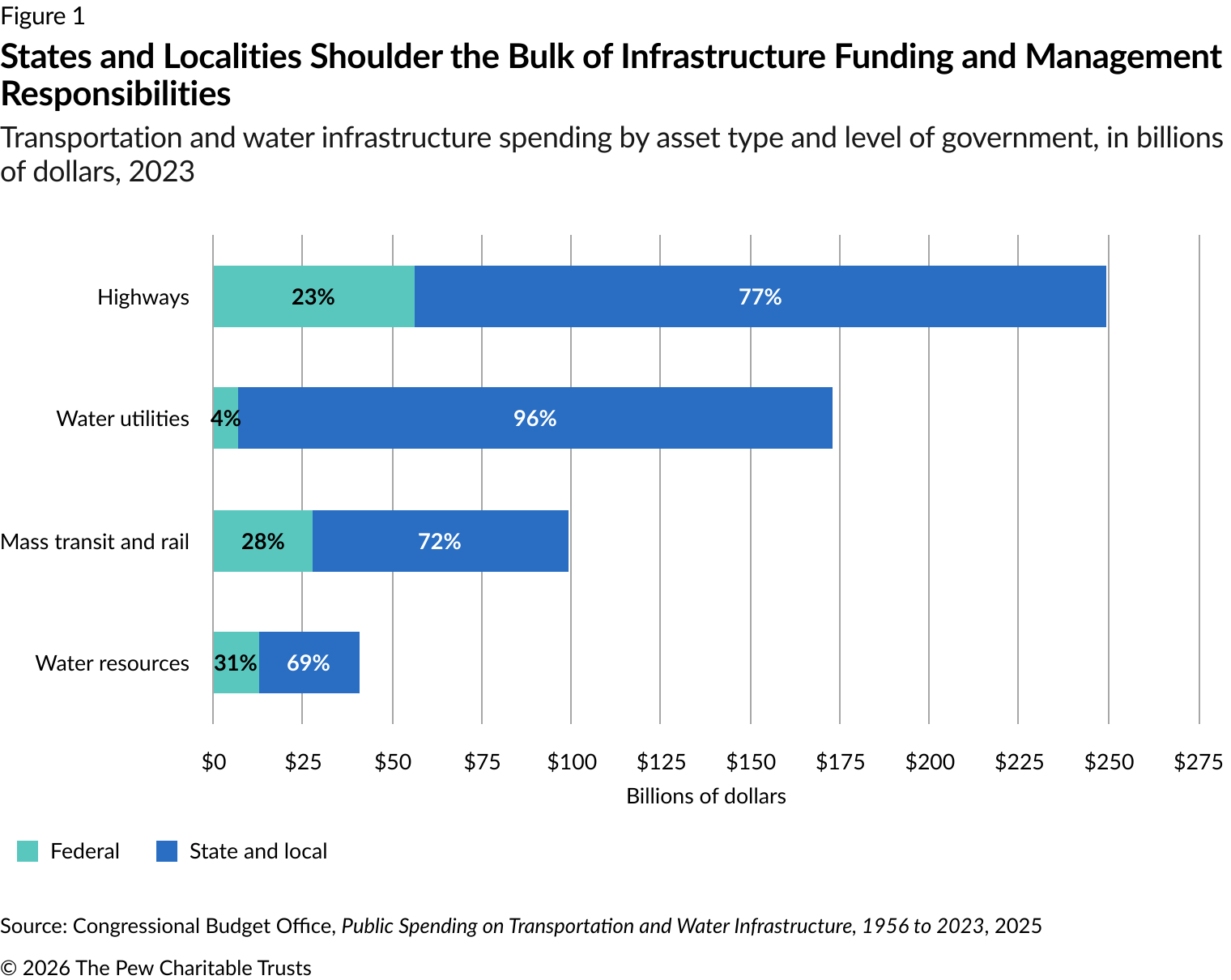

As the historic federal funding provided under the 2021 Infrastructure Investment and Jobs Act begins to taper off, state and local governments—which own or operate most of the nation’s public roads, bridges, and water systems—face growing pressure to sustain the investments that began with those federal dollars and manage ongoing maintenance costs. (See Figure 1.)

But this isn’t just a funding problem. Infrastructure responsibilities are fragmented across thousands of local governments with varying levels of fiscal capacity and expertise. And in many cases, states bear the fiscal and economic consequences—through spending on emergency aid, regulatory compliance, or disaster recovery—when locally managed roadway and water assets fail. Infrastructure outcomes depend not only on how much money is available, but also on whether states and localities can coordinate effectively on planning, prioritizing investments, and managing assets across systems.

To help meet this challenge, states are turning to various centralized financing institutions that they have long relied on to assist local governments in accessing capital markets and federal funds for infrastructure: municipal bond banks, state infrastructure banks, and other independent entities. In recent years, several states have expanded these entities’ roles to include helping local governments build planning, asset management, and data-sharing capacity; exercising oversight over struggling locally managed water systems; and filling gaps in resilience financing and disaster recovery for core transportation and water infrastructure.

About state financing entities

Policymakers and infrastructure agencies often view state financing institutions in terms of the different tools they provide, but with their long history of supporting local governments, they can also play a broader role by helping to coordinate planning and asset management so that infrastructure investments can be distributed and managed more effectively across jurisdictions. Understanding these entities’ backgrounds and original mandates can help state leaders identify the right institution for each of their infrastructure needs and challenges:

- Municipal bond banks pool borrowing needs across local governments into single bond issuances. This enables participating localities to leverage the state’s credit—which is typically stronger than the individual jurisdictions’—to secure lower interest rates and more easily access capital markets.

- State infrastructure banks (SIBs) were created through a Federal Highway Administration pilot program in 1996 and function as revolving loan funds that recycle repayments into new loans. Many SIBs still focus on major highway projects, but some states have expanded the model to broader water, energy, and resilience investments. These state-capitalized revolving-loan funds are distinct from federally resourced state revolving funds for drinking and wastewater infrastructure, although some SIBs also help administer those programs.

- Other independent authorities can act as oversight bodies that monitor local government and utility fiscal health and intervene when infrastructure systems are at risk. North Carolina’s State Water Infrastructure Authority and South Carolina’s Rural Infrastructure Authority illustrate this approach: By leveraging the relationships they’ve already established with local governments and utilities through their funding programs, they are able to identify potentially struggling systems and offer technical assistance.

Capital planning, asset management, and data-sharing capacity

Perhaps the most significant expansion of these infrastructure financing authorities’ roles has been into pre-project technical assistance and capital planning support, where they are helping local governments develop asset inventories, improvement plans, and project pipelines before borrowing or applying for grants. For many smaller jurisdictions, the barrier is not unwillingness to invest but limited administrative capacity to plan for, prioritize, and pursue funding or financing.

For example, Vermont’s Bond Bank convenes an annual Capital Planning Forum with the University of Vermont’s Leahy Institute for Rural Partnerships, bringing together local officials, state agencies, and financing experts to strengthen local planning capacity. The bond bank has also built a geographic information system-based local infrastructure database that maps 20 years of financing data statewide to help communities understand past investment patterns, and it has provided the state Legislature with historical facilities data to inform school infrastructure planning.

Rhode Island’s Infrastructure Bank (RIIB) takes a complementary approach, offering technical assistance and several planning grants to help communities assess risks and develop project pipelines before they borrow, directly tackling a persistent problem: Many communities that have recognized needs lack a pipeline of “shovel-ready” projects to address them.

Support for local fiscal distress

North Carolina’s State Water Infrastructure Authority provides help for struggling water utilities through the Viable Utility Program, which it runs in partnership with the Local Government Commission, an entity within the state treasurer’s office that monitors and assists financially distressed local governments. Program administrators can draw funds from the Viable Utilities Reserve to provide grants for infrastructure condition assessments and rehabilitation projects, operations, and other activities for water utilities that the authority and the Local Government Commission have designated as distressed. To receive funding, the program requires utilities to complete asset assessments, develop action plans, and participate in training, directly tying financial oversight to infrastructure planning.

South Carolina’s Rural Infrastructure Authority plays a similar role in assessing and supporting struggling water utilities. In 2022, it completed a statewide water utility viability assessment and in 2025 launched a pilot Viability Improvement Program to deliver technical and capital assistance to small utilities.

Resilience and recovery

States are increasingly turning to financing authorities to invest in resilience ahead of disasters and manage costs after they occur, especially as federal support becomes less certain.

For example, since 2018, RIIB’s Municipal Resilience Program has helped all of Rhode Island’s 39 municipalities identify risks and develop project pipelines—such as culvert upgrades, pump station improvements, and flood-proofing of critical facilities—but the state only provided funding for resilience efforts on a case-by-case basis through voter-approved green bonds issued by RIIB. Then in 2025, the state established the Resilient Rhody Infrastructure Fund, a state-capitalized revolving loan fund to deliver more easily accessible and reliable financing for municipal resilience projects statewide. With the future of FEMA’s Building Resilient Infrastructure and Communities and other federal programs in doubt, Rhode Island has shown how states can build durable local capacity.

After disasters occur, municipalities often must cover immediate and significant costs to repair essential infrastructure, sometimes totaling several times their annual budgets, before they can receive federal reimbursements. To help local governments meet these obligations, Vermont’s Bond Bank—in the wake of major flooding in 2023—launched a short-term disaster bridge loan program, leveraging its existing lending relationships and its statewide role to help state and local officials quickly coordinate on recovery options and to provide needed bridge financing.

Match tools to statewide needs

Of course, no single model fits every state. States with many small or rural governments may benefit from pooled borrowing and technical assistance through bond banks, while larger states may rely more on the cross-agency coordination that statewide infrastructure banks can offer. In some states, financing authorities that already play an oversight role can also help coordinate planning, financing, and recovery efforts when infrastructure systems are at risk. But regardless of which tool a state uses, the goal is the same: Building the capacity and statewide coordination to manage infrastructure as a long-term fiscal commitment, before costs escalate or systems fail.

Fatima Yousofi is a senior officer and Logan Timmerhoff is an officer with The Pew Charitable Trusts’ state fiscal policy project.

People