States With Automated Retirement Savings Programs See Growth in New Private Plans

New data shows private-sector retirement plans increase in number after adoption of state-run auto-IRAs

Overview

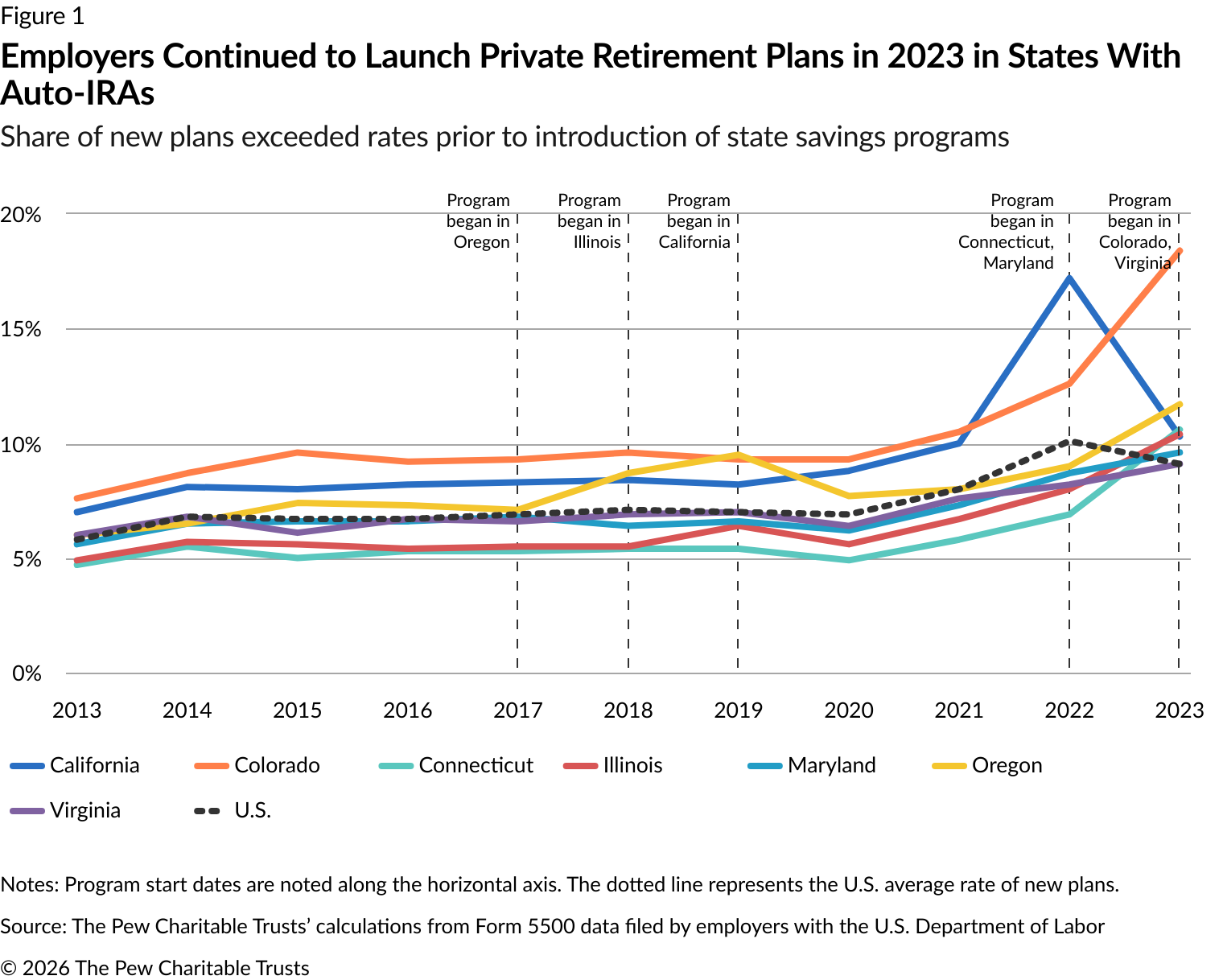

In 2023, private businesses in California, Colorado, Connecticut, Illinois, Maryland, Oregon, and Virginia created new retirement plans at rates similar to or greater than the national average—in some cases, several years after the state had implemented a state-facilitated automatic enrollment workplace savings program (auto-IRA). In fact, nearly every state with an auto-IRA program recorded an increase in the rate of new private-sector retirement plans from 2022 to 2023.

This research suggests that state-facilitated savings programs continue to complement the private retirement plan market and do not inhibit or compete with private plan formation, even years after a program goes online.

Nationally, the share of all private retirement plans that were new fell from 10.1% to 9.1% from 2022 to 2023. In states with active auto-IRA programs, new private plans comprised between 9.1% (in Virginia) and 18.4% (in Colorado) of all private plans. States with automated state-run plans saw year-to-year increases in the new plan share that ranged from 0.9% in Virginia and Maryland to 5.9% in Colorado, with the exception of California, which saw a decrease in new plans following a surge in 2022.

Among states without auto-IRA programs, Wyoming had the highest rate of private plan formation in 2023, with 13.3%. West Virginia was lowest, with 5.4%. Every state with an auto-IRA program had a rate of private plan formation at or above 9% in 2023, with Colorado claiming the top spot nationally. Colorado’s share of new plans rose to 18.4% from 12.6% the year prior, coinciding with the implementation of its auto-IRA program. All states saw an increase in the share of new plans in their state immediately following implementation of their automated savings program (Figure 2).

As of February 2026, 17 states have adopted auto-IRA programs. Fifteen of those programs are actively enrolling participants. Across the 12 active states for which data was available, more than 1.19 million funded accounts had amassed over $2.89 billion in assets.2

The Pew Charitable Trusts has been tracking the formation of private-sector retirement plans since 2021. Pew initially examined data from annual filings by employer-sponsored retirement plans to the U.S. Department of Labor from 2013 to 2019.3 That analysis suggested that, in states with auto-IRA programs, employers with retirement plans continued to offer them, and businesses without plans were adopting new ones at rates similar to those before the state options became available.

The data comes from federal Form 5500 annual reports, which are a required regulatory filing to the Department of Labor for sponsors of retirement benefit plans. Pew drew on data from Form 5500s and Form 5500-SFs (short forms, which are typically used for plans with fewer than 100 participants) filed between 2013 and 2023. Any business that indicated it had a retirement plan was included for each plan year it had a retirement plan.

In previous Pew analyses, states that enacted auto-IRA legislation saw increases in new private-sector retirement plans after the enrollment deadline or launch of the state program.4 In 2023, well-established states such as Oregon (which began enrolling participants in 2017) and Illinois (2018) saw increases in the rate of new retirement plans (Figure 1). California was the only auto-IRA state that saw its share of new private plans drop in 2023; still, the 10.3% of retirement plans that were new was higher than it was in every year from 2013 to 2019, when California implemented its automated state savings program. From 2013 to 2018, California’s average new plan rate was 8%.

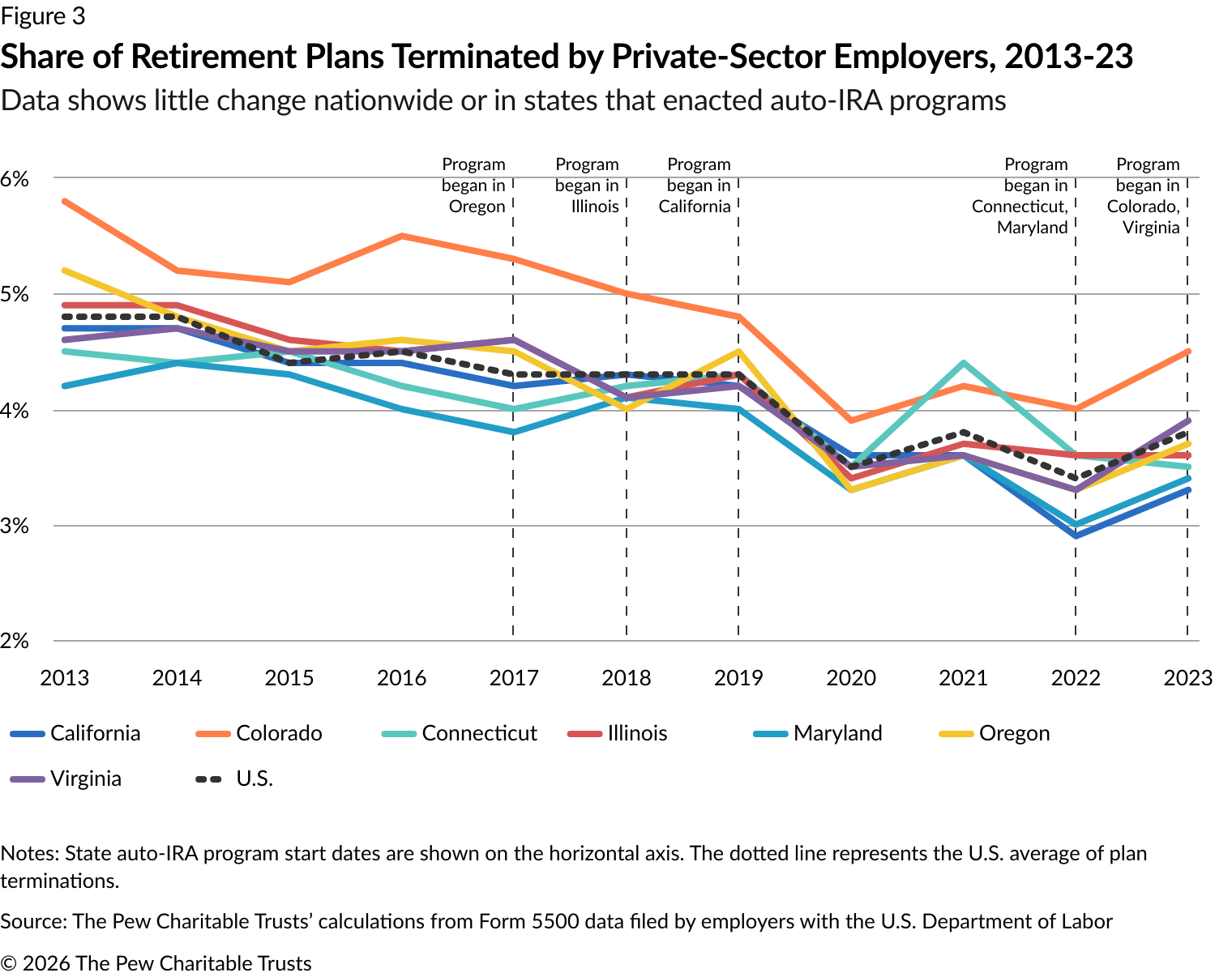

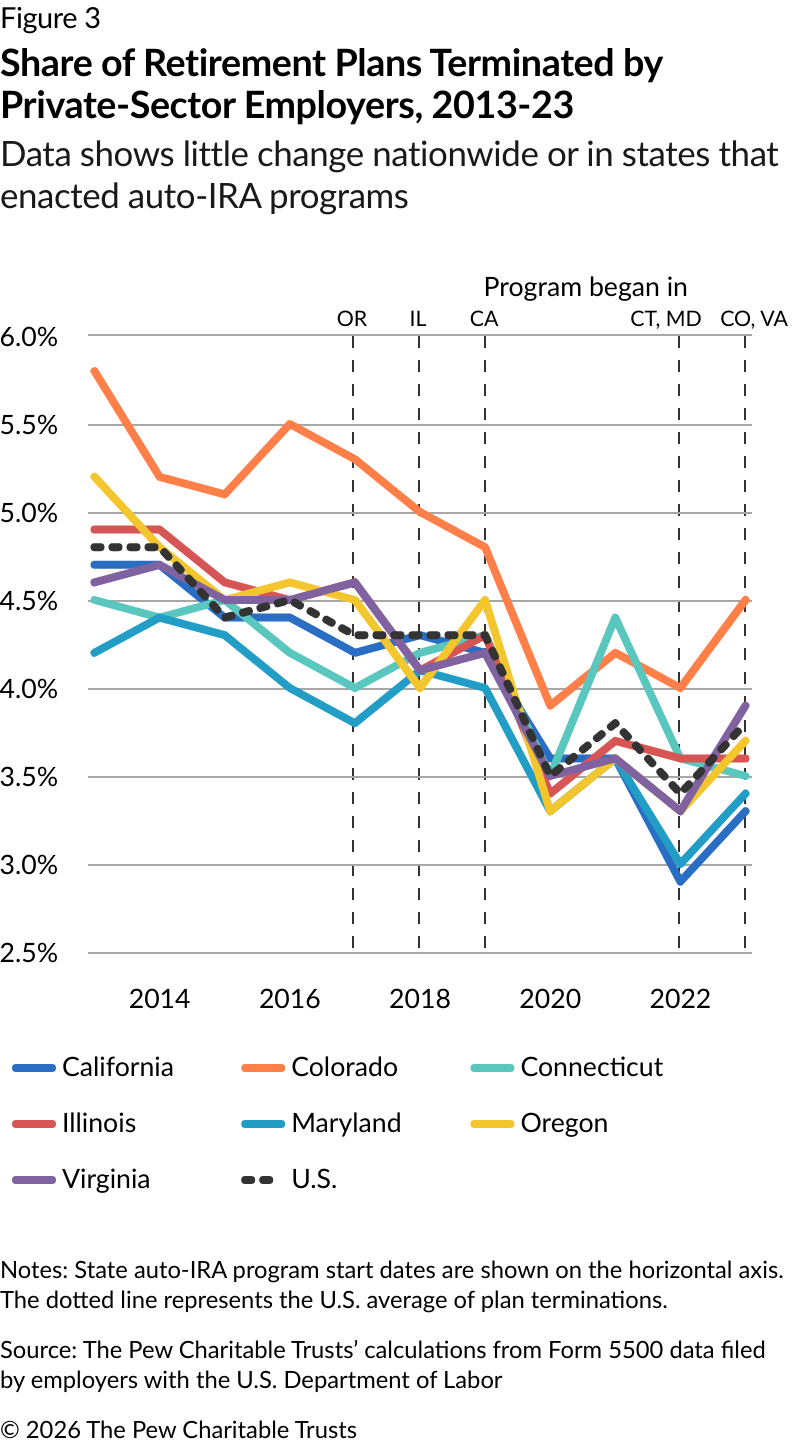

Moreover, rates of private plan terminations in states with automated savings programs were, with one exception, at or below the national average (Figure 3). Colorado had higher rates of plan termination than the national average in every year from 2013 to 2023. Colorado began enrolling workers in its state auto-IRA program in 2023.

Some policymakers have expressed concern that state auto-IRA programs might crowd out private market plans. As Pew’s data shows, however, the opposite occurs: States with auto-IRA programs have seen increases in private-sector retirement plan creation, often at rates that are significantly higher than in states without auto-IRAs.

California illustrates this trend of new plan creation. Although California’s share of new plans fell in 2023, this decline followed a dramatic spike in new plan creation in 2022. In 2022, the share of private retirement plans that were new in California increased to 17.2%, from 10% in 2021. This increase occurred because more than 220,000 employers became eligible to join the state’s auto-IRA program, CalSavers, a portion of which opted to adopt their own plans. In 2023, California returned to a new plan creation rate that was similar to 2021, though still above the new plan creation rate before California instituted its automated savings program in 2019. Data from financial services firms corroborates these findings in California. For example, Gusto, a payroll and benefits provider that serves more than 400,000 businesses in the U.S., had an increase in new private plan adoption associated with the 2022 compliance deadline in California for its smallest employers.5 Gusto’s experience as a private 401(k) provider highlights how state automated savings programs may spur businesses to adopt their own plans.

Nationally, 10.1% of all retirement plans were new in 2022, an increase from 8% the prior year. Several factors likely led to the 2022 spike. The passage of the federal SECURE (Setting Every Community Up for Retirement Enhancement) Act in 2019 and SECURE 2.0 Act in 2022 offered new incentives for small businesses to start retirement plans; smaller employers are less likely to offer retirement benefits due to cost and administrative challenges.6 Moreover, new forms of group plans, known as pooled employer plans, or PEPs, were created by the Secure 2.0 Act; the marketing of PEPs may have contributed to the 2022 increase. The availability of PEPs and new tax incentives may have had a short-term impact on new plan formation, with 2023 data showing a nationwide decline. States with auto-IRAs may be seeing increases in private plan formation due to employers adopting new plans rather than enrolling in their state’s automated savings programs, according to data from Gusto.

Employers may opt to start their own plan rather than participate in their state’s automated savings program for a number of reasons. For example, state automated savings programs are prohibited from offering an employer match, which provides a greater financial benefit to workers and may be seen as an employee retention tool. The state programs may nudge those businesses that had been considering adopting a program to finally do so in order to offer a plan that gives them an advantage over employers that use the automated savings program.

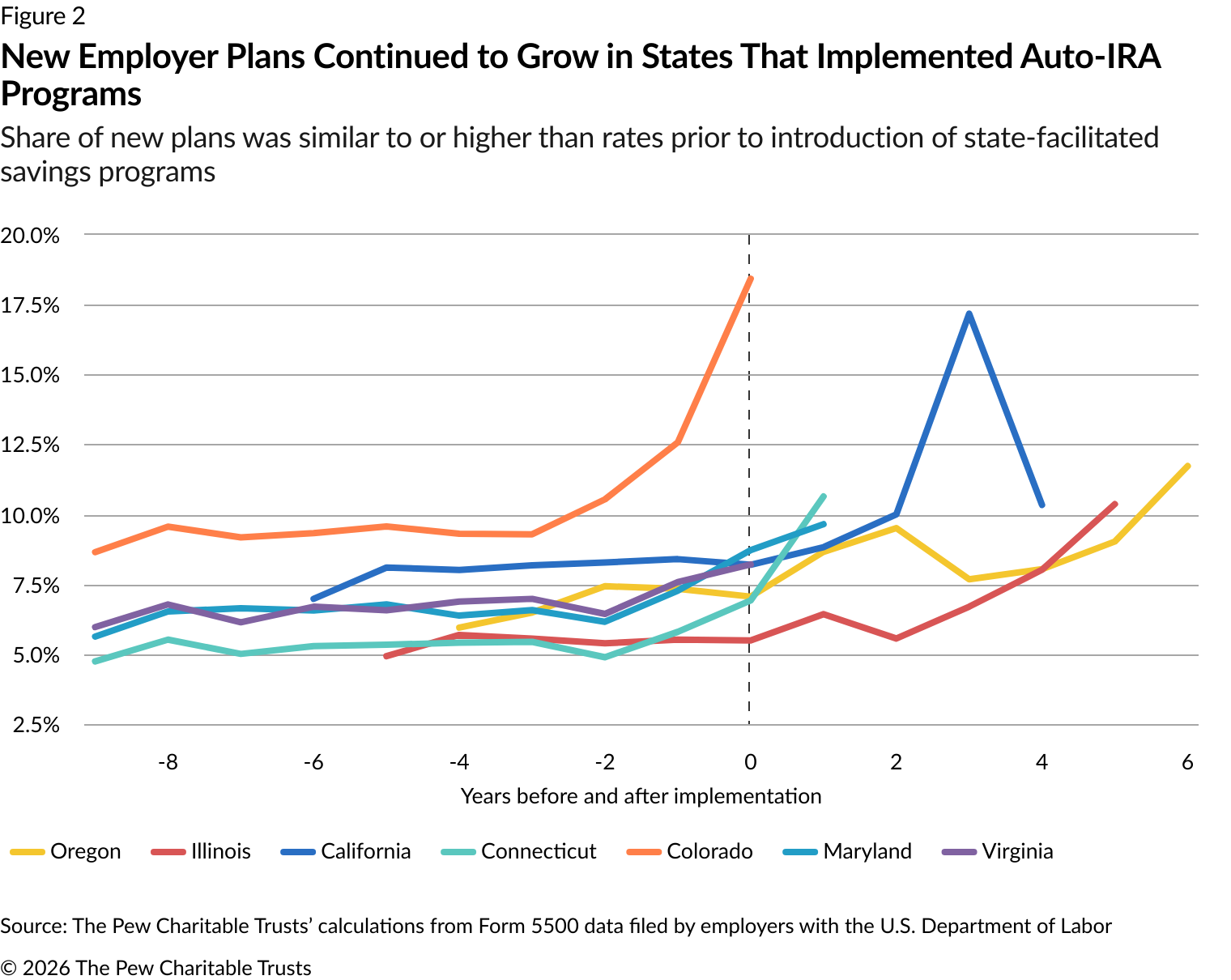

Figure 1 does not fully capture the effect of new auto-IRA programs, as states had different starting dates and some states rolled out their programs over several years. Figure 2 looks solely at states with operational auto-IRA programs, adjusting the horizontal time scale so that state data is pegged to the program start date (year 0 in the graph). As such, year 0 on the chart below represents the start of each state’s program, with the data to the right representing how many private plans were created after the auto-IRA’s formation.

States with auto-IRA programs saw higher rates of new private plan formation at or after year 0, followed by a decline in some states as the programs were implemented. This increase would be expected at the start of an auto-IRA program, because eligible employers must either register for the state program or start their own plan. With time, fewer employers are affected by the auto-IRA programs, so the share of new plans drops. One exception was Oregon, which had an extended rollout of its program and saw extended growth in new plans over time (yellow line in Figure 2).

To fully understand the effect of state-facilitated auto-IRA programs on private employer retirement plans, Pew looked at whether and how often employers terminated retirement plans because the state auto-IRA became an option. As shown in Figure 3, the rate of plan terminations nationwide rose by 0.4 percentage points between 2022 and 2023 (from 3.4% of plans to 3.8%). Terminations also rose in five states with automated savings programs (California, Colorado, Maryland, Oregon, and Virginia). Still, terminations in these states were generally in line with the national trend, rising between 0.4 and 0.6 percentage points; Connecticut and Illinois were exceptions, with both recording similar rates of termination in 2022 and 2023. Colorado was the only state with an auto-IRA program that had a private plan termination rate that significantly exceeded the national average in 2023; it has been above the national average every year since 2013. These results show that employers in states with auto-IRA programs are not canceling their retirement plans at higher rates than the national average.

This evidence from California, Colorado, Connecticut, Illinois, Maryland, Oregon, and Virginia continues to indicate that auto-IRAs complement private-sector retirement plans such as 401(k)s rather than crowding them out. Similar results have been found in industry data (like that from Gusto) as well as in other research.7

At the same time, auto-IRAs allow private businesses that cannot afford their own retirement plans to take advantage of a no-cost, basic savings program for their workers. Further research and study will help clarify how employers and plan sponsors respond to these initiatives in states that implement new auto-IRA programs.

How the retirement plan adoption and termination rates were calculated

The data in this report comes from federal Form 5500 annual reports, which private sponsors of retirement savings plans must file annually with the U.S. Department of Labor. Using benefit codes provided by filers, Pew researchers limited the review to employers that offer retirement plans, including defined benefit and defined contribution plans. Plan sponsors are required to file just once per plan per year; a plan with participants in several states would be represented only in the state where it was filed even though it includes workers in additional states. If employers filed multiple times for the same plan within a state, or across several states, researchers used the form signature date to keep the most recent filing and drop earlier ones. If the signature date was missing, a default duplicates drop procedure was used. Cases in which a single filing was reported as both an initial filing and a plan termination were dropped.

Instead of relying on whether firms ticked boxes on Form 5500 to indicate an initial or final (termination) filing for a pension plan, Pew reviewed each plan’s filings year by year to ascertain whether a given filing was indeed the first or last during the period from 2013 to 2023. For initial filings, Pew adopted a five-year look-back (to 2009 filings). For final filings, Pew adopted a two-year look-forward through 2021 and then relied on ticked Form 5500 filing-type boxes for 2022 and 2023 (the last available year of data).

Plan initiations and terminations can be affected by the general business climate and other economic factors not explicitly controlled for in this analysis. New plans may include both new businesses as well as businesses that have been in operation for years and are just starting a retirement plan. Terminations may include businesses that have ceased operations or merged with another business or plans that have been merged into another plan.

The Department of Labor’s Form 5500 data is updated regularly, typically around the beginning of each month. The data used for this report, from 2013 through 2023, was downloaded in January 2025.

Endnotes

- Theron Guzoto, Mark Hines, and Alison Shelton, “State Automated Retirement Programs Don’t Crowd Out Private Plans,” The Pew Charitable Trusts, 2024, https://www.pew.org/en/research-and-analysis/articles/2024/11/14/state-automated-retirement-programs-dont-crowd-out-private-plans.

- “State Program Performance Data,” Georgetown University Center for Retirement Initiatives, https://cri.georgetown.edu/states/state-data/current-year/.

- John Scott, “Availability of State Auto-IRAs Appears to Complement Private Market for Retirement Plans,” The Pew Charitable Trusts, 2021, https://www.pew.org/en/research-and-analysis/articles/2021/06/17/availability-of-state-auto-iras-appears-to-complement-private-market-for-retirement-plans.

- Theron Guzoto, Mark Hines, and Alison Shelton, “State Retirement Programs Don’t Crowd Out Private Plans.”

- Steve Abbott, “State Auto-IRAs Can Boost 401(k) Adoption,” Gusto, 2022, https://gusto.com/resources/gusto-insights/stateautoiras401ks.

- The Pew Charitable Trusts, “Employer Barriers to and Motivations for Offering Retirement Benefits,” 2017, https://www.pew.org/-/media/assets/2017/09/employer_barriers_to_and_motivations.pdf.

- Sita Nataraj Slavov et al., “How Do Firms Respond to State Retirement Plan Mandates?” revised 2024, https://www.aei.org/researchproducts/working-paper/how-do-firms-respond-to-state-retirement-plan-mandates.

People